What Are Soft and Hard Credit Checks?

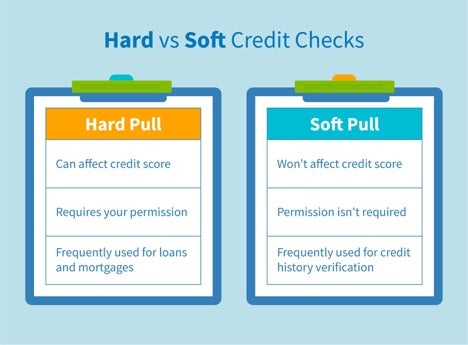

The short answer: soft credit checks don’t affect your credit score and hard credit checks do.

What is a Soft Credit Check?

A soft credit check or "soft pull" happens when you view your own credit report or your credit is checked by a potential employer or landlord. It also occurs when credit card and insurance companies send pre-approval offers. Soft credit checks don't affect credit scores because of their frequency and non-exchange of funds.

What Does a Soft Credit Check Show?

Each soft pull stays on your report for a maximum of two years and appears in the section of your report marked “soft inquiries” or “requests viewed only by you.” Soft credit checks also show the following:

- Open loans and lines of credit

- Payment frequency

- Accounts in collections

- Other public records under your name

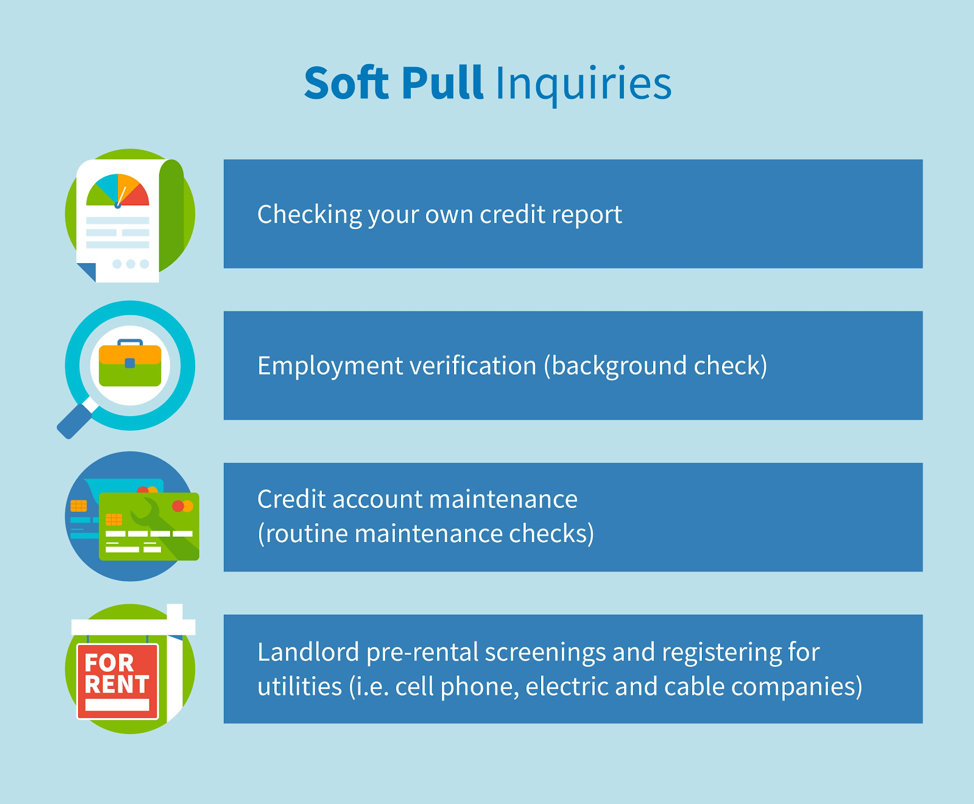

Who Uses Soft Credit Inquiries?

Soft credit checks occur more than most people realize. Like we said above, these inquiries don’t affect your credit score, but it’s important to know when a soft credit pull can appear on your report.

- Checking your own credit report

- Employment verification

- Pre-screening by creditors

- Credit account maintenance

- Landlord pre-rental screenings or registering for utilities

When it comes to employment opportunities, soft inquiries let companies know your credit history and status. Professions in finance, high-end retail, law enforcement, confidential security and government require mandatory credit checks. Employers that perform inquiries before employment must follow the guidelines of the Federal Fair Credit Reporting Act (FCRA).

How Do Soft Credit Checks Impact Your Credit Score?

A soft credit check is a snapshot of your credit history and a key factor in how your credit limit is determined. Regular maintenance updates and removes old case information, such as paid-off debts and loans or former Chapter 13 bankruptcy.

Most people want these negative items removed as soon as possible so that their credit score increases. However, the credit bureaus don't update reports every day. Balances are reported near the end of a customer's billing cycle.

What is a Hard Credit Check?

A hard credit check or "hard pull" happens when you apply for a loan, mortgage or other major financial transaction and you give a financial institution approval to view your credit report. A hard credit check does affect your credit score because it represents a request for funds and the accumulation of more debt.

What Does a Hard Credit Check Show?

Hard inquiries show similar information to soft inquiries, but all of the companies that view your credit report must have your consent. Hard inquiries appear in the section of your report marked "inquiries shared with others."

Who Uses Hard Credit Checks?

Hard credit checks occur less than soft checks. As stated, hard pulls are only allowed when you grant permission to a financial institution or lender.

Hard inquiries are conducted by:

- Mortgage companies

- Auto financing firms

- Credit card companies (new accounts and increases in lines of credit)

- Student loan companies

- Financial lenders (personal and business loans)

Unlike soft inquiries, hard inquiries will affect your credit score. A few pulls within a short period of time may not lower your score, but frequently applying for credit cards in a short period of time can drop your score five to 10 points (yikes).

How Do Hard Inquiries Affect Your Credit Score?

People cringe when a hard inquiry appears on their reports. The assumption that lenders make is that you're seeking additional financing because of a lack of funds in your bank account. Frequently applying for new credit cards or requesting increases in lines of credit are red flags.

The good news is that if you’re "rate shopping" for a new home or car, or applying for a personal loan, there’s a window of 14 to 30 days when multiple hard checks are seen as a single inquiry.

How to Dispute Hard Inquiries

Despite increases in credit security, it’s not completely uncommon for unauthorized hard inquiries to appear on your credit report. Sometimes it’s a reporting error, but sometimes it’s a sign of identity theft.

In 2018, 1.4 million fraud reports were processed, racking up $1.48 billion in losses. It's recommended that you frequently check and maintain your credit report. Here are a few tips for how you can catch unapproved hard inquiries:

- Review your credit report frequently. Take note of all the companies that have viewed your credit report and ensure that you authorized the hard checks on your account.

- File a hard inquiry dispute letter. If you notice anything unusual, immediately report it to the credit bureaus—Equifax®, Experian® or TransUnion®—and request to have it removed. Although these credit bureaus are the primary credit overseers, creditors are not required to report your history to all three. In this case, the inquiry may appear on some and but not all of the bureaus' reports. Keep documentation of the incident and all correspondence between you, the credit card company or lender in question.

How Often Should You Check Your Credit Report?

You can request a free copy of your credit report from each of the credit bureaus once a year, although we recommend that you review them quarterly throughout the year. This will let you check and compare credit scores from all, especially before making any major purchases. When in doubt, contact a credit professional for assistance.

If you need help, call the credit experts

learn moreFICO and “The score lenders use” are trademarks or registered trademarks of Fair Isaac Corporation in the United States and other countries.

** Your results will vary