Disclosure regarding our editorial content standards.

Turning 18 is a huge milestone: You’re likely preparing to go off to college or trade school, planning out your gap year or applying to jobs. Your finances are an incredibly important aspect of your life—from student loans and rent to being in charge of your budget for the first time. You’ve probably been hearing about credit and how important it is as well.

Because building good credit takes time, it’s essential to start at a young age to help secure low-interest loans on mortgages, cars and other assets in the future. Below, we discuss seven ways to build credit at 18 so you can set yourself up for financial success at a young age.

1. Understand what makes up your credit score

When it comes to understanding credit, it can feel overwhelming at first—what’s your credit score? How do you calculate debt-to-income ratio? What does APR mean?

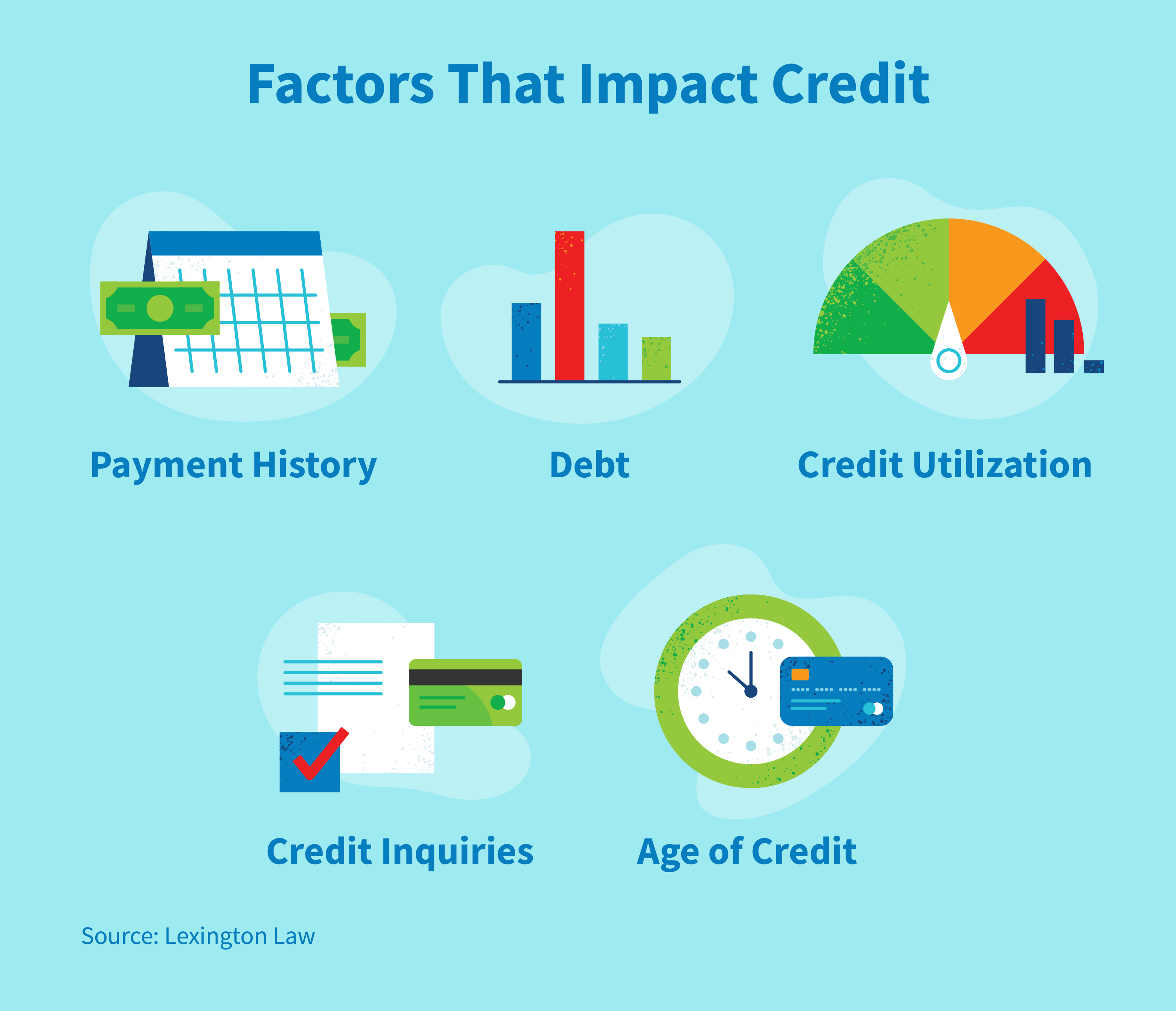

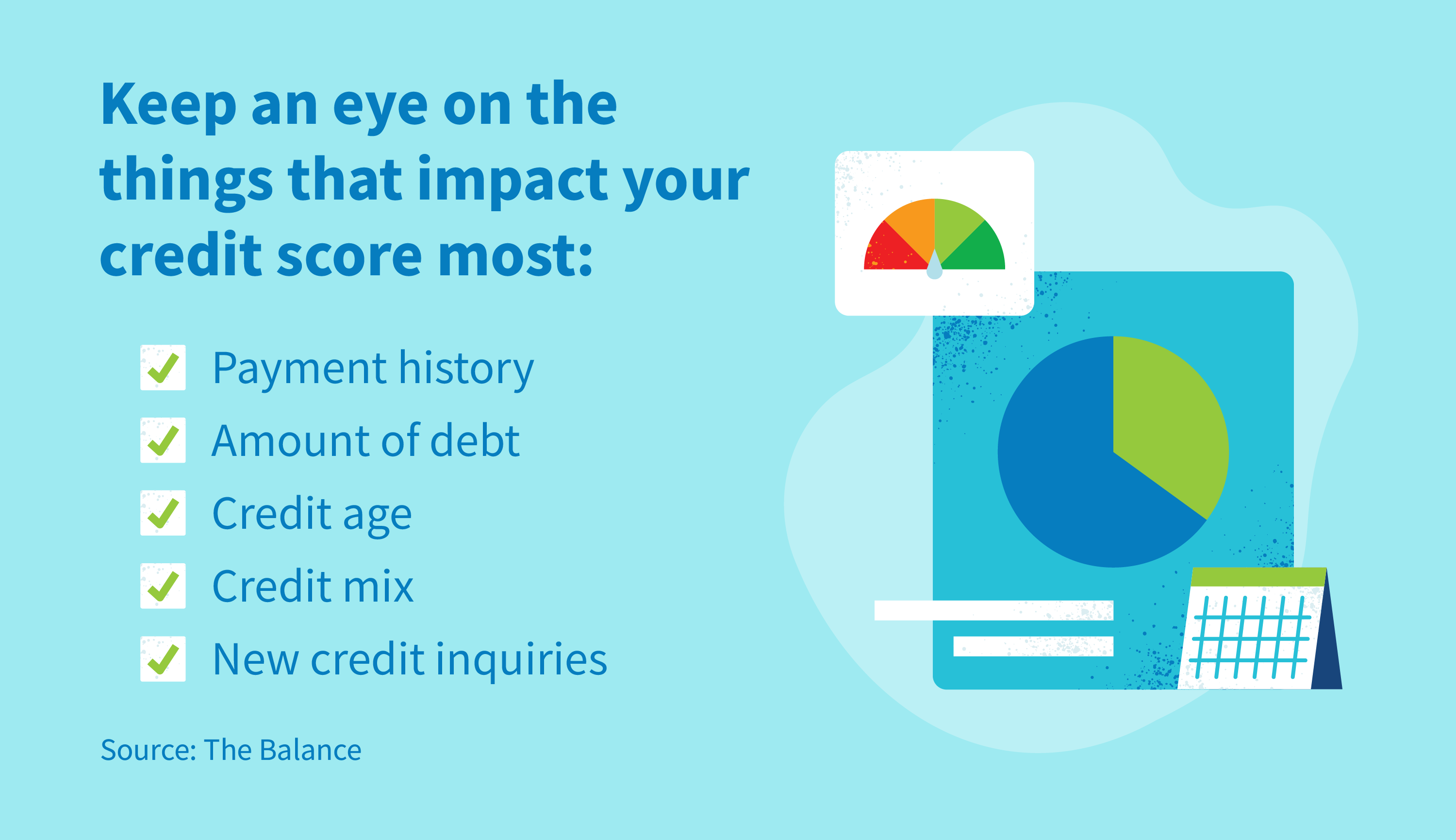

Take a deep breath! You don’t need to memorize everything on day one. Credit health is a lifelong practice, so lace up your shoes—this is a marathon, not a sprint. Thankfully, it’s easy enough to start with the basics to get started on the right foot. There are a few distinct factors that are important to think about when building credit:

- Payment history: Paying bills on time is important for many reasons, from keeping interest rates low to establishing good credit. Payments that are 30 days or more late will have a negative impact.

- Credit utilization: This is the ratio of your outstanding credit card balance to your credit card limits. Low credit utilization is ideal—it shows that you’re only using a small amount of credit loaned to you. Try to use 30 percent or less of your available credit at a time.

- Age of credit: The longer you’ve had credit, the better you’ll look to lenders. They want to see someone with an established credit history, which ties into your payment history and credit utilization. This one will be trickier to nail when you first get started, but we have some tips later about how to help this aspect of your credit.

- Debt: Carrying a good deal of debt can greatly affect your score and ability to get approved for loans in the future.

- Inquiries: It’s best to limit the number of credit inquiries you have if you want a good score. There are two types: soft and hard. A soft inquiry is when your credit is pulled as part of a background check, typically by you or another person, and it won’t affect your score. A hard inquiry occurs when a financial institution checks your credit for a lending decision like a loan or mortgage. You have to authorize hard inquiries, and they can negatively affect your credit score if performed often.

Even though it’s difficult to build credit when you don’t have various lines of credit and you’re just getting started, there are steps you can take to show lenders that you’ll be responsible with a loan.

2. Become an authorized user

One of the most effective ways to start building credit at a young age is to become an authorized user on a friend or family member’s account. The primary cardholder simply adds your name to the credit card account, and you have the ability to make purchases with that card. Even if you don’t use the card, the account can still go onto your credit report and help build your credit score, as you benefit from the age of that account.

It’s important to make sure the primary account holder has responsible financial habits. If they acquire too much debt or fail to make payments on time, this could damage both parties’ credit scores. You’ll also want to make sure the credit card company reports card activity for authorized users beforehand or else you won’t benefit.

3. Take out a (small) loan, like a credit builder loan

While we don’t recommend taking on debt simply to build credit, if you have a valid reason to take out a small loan—like a student loan—it’s a helpful way to build on your short credit score history and prove that you can handle debt.

However, if you do take out a loan, we recommend it be small—maybe a few thousand dollars—and you must make payments on time each month. This helps legitimize your case as a consumer who can make payments on time and thus is a good credit risk.

A credit builder loan is an option offered by smaller financial institutions like credit unions and community banks. Because they are designed to help people who have bad or little to no credit, the amount borrowed is held in a bank account while you make payments and build credit. Once the loan is paid off, then you receive the money. For this reason, you need to prove you have income to afford the payments, so it’s safest to choose a low loan amount.

4. Open a credit card

Without any credit history whatsoever, it’s hard to qualify for a credit card, but there are a few options. If you’re opening a credit card, the most important factor is making on-time, monthly payments to prove you are trustworthy to lenders. Below are a few credit card options to explore:

- Unsecured credit cards: These are the most common type of credit cards. They don’t require a security deposit to be approved or to get your limit increased, but they usually present you with a credit limit based on your creditworthiness before you apply.

- Secured credit cards: These require up-front security deposits to open, and that deposit typically equals your initial credit limit.

- Student credit cards: If you’re enrolled in school, this could be a viable option. These cards typically have low credit limits, but high interest rates for those that don’t pay on time. Often, they even offer incentives for good grades.

5. Make payments on time

One of the most important things you can do to build credit is to make timely payments, as payment history makes up 35 percent of your credit score. This is the case for every type of payment you have, from a cell phone service to a car payment.

You can stay on top of these by setting due-date reminders on your phone, or taking it a step further and scheduling automatic payments each month. When building credit, your number one goal should be to never miss a payment.

6. Regularly check your score

We recommend monitoring your credit reports and credit score regularly as this will help you better understand what will positively and negatively affect them, and, in turn, allow you to build better credit based on these findings.

For example, did your credit drop a significant amount due to a missed payment? The best way to learn what affects your credit score is to continuously monitor and note when it goes up or down. This also helps you catch signs of theft if you notice any inconsistencies.

7. Don’t get too zealous

It’s always a good idea to pause and think about what you truly can and cannot afford. The more credit cards and loans you open, the greater the risk that you’ll fall into debt and negatively affect your score.

As a young spender who is just starting out, we recommend managing just one credit card and/or small loan until you understand how things work. Starting small will help ensure that you don’t ruin your credit from the beginning and have to retroactively go back and fix it. As time goes on, you can add other lines of credit into the mix and begin diversifying your credit profile.

While starting to build your credit may seem like a long and daunting task, there are ways you can begin establishing a positive credit history, even as young as 18. Utilize the above tips and continue to educate yourself on how to build credit so that you can purchase your dream car at an affordable rate sooner rather than later.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263