Disclosure regarding our editorial content standards.

Credit insurance is a type of insurance that covers missed payments on your loan or credit card due to situations like death, disability, unemployment, destruction or loss of property. There are various types of credit insurance to cover all of these things and more.

Policies are available for many things—like that auto loan for your brand-new ride—but you’ll probably see credit insurance more often as an optional feature for credit cards. Credit insurance can give you peace of mind if you miss a payment for reasons beyond your control, but it may end up costing you more in the long run.

Let’s think about the situations we mentioned above (death, disability, etc.). When any of these things happen and you’re unable to make your loan payments, that’s when credit insurance kicks in to cover for you.

Lenders can sell you a credit insurance policy and may include it in your loan paperwork. However, lenders are required to clearly disclose to you if they included credit insurance and other optional products in their contract, according to the Federal Trade Commission (FTC). Also, lenders can’t deny you credit if you don’t buy their credit insurance.

Credit insurance types

There are five main types of credit insurance:

- Credit life insurance: This insurance pays your remaining loan balances to your lenders if you pass away.

- Credit disability insurance: This covers payments if you’re sick or hurt and can’t work, and it’s also called accident and health insurance.

- Credit unemployment insurance: If you’re unwillingly unemployed due to getting laid off or another circumstance that isn’t your fault, this type of insurance covers payments to your lender. This is also known as involuntary loss of income insurance.

- Credit property insurance: This protects personal property used as collateral for a loan if your things are damaged, stolen or otherwise lost through a natural disaster or accident.

- Trade credit insurance: This insurance covers businesses that sell services and goods on credit. It protects businesses when a customer doesn’t pay, like if they can’t afford the charges.

Depending on the credit insurance plan you’re looking at and your credit health, the cost of a policy can vary, which we’ll cover next.

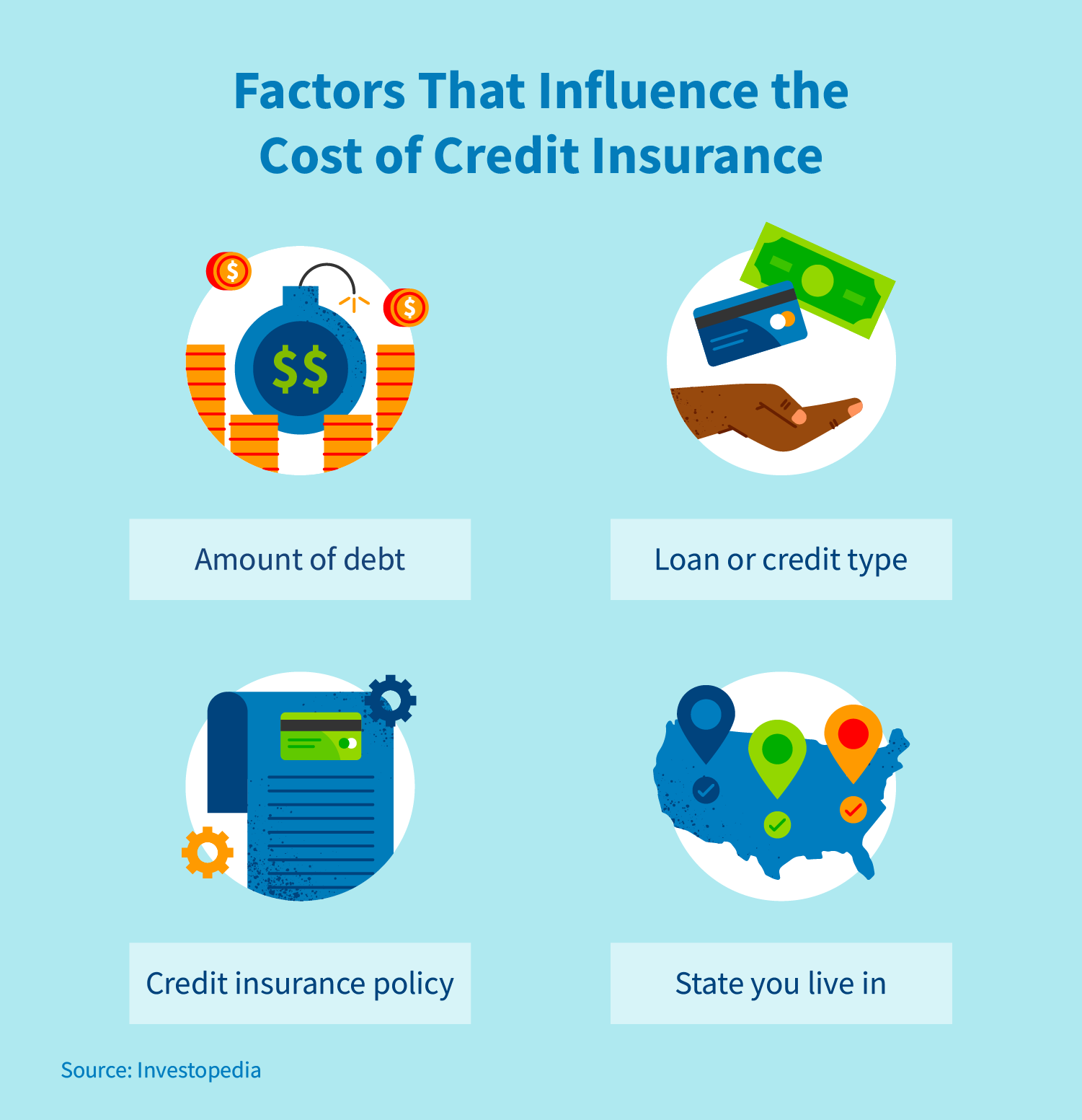

Credit insurance cost

Like other insurance policies, the cost of credit insurance varies based on a few things, including the amount of debt you’re protecting, your loan or credit type, your credit insurance policy and your home state.

Let’s look at an example: If you’re 30 years old and in good health, credit insurance can cost you $370 for $50,000 of coverage, according to the State of Wisconsin Department of Financial Institutions.

The way you pay these costs depends on if you’re insuring open-end or closed-end debt. Although we’re describing how charges are normally applied to these types of debt, check the credit insurance’s terms so you know how charges work for that policy.

Open-end debt

Open-end debt allows you to borrow multiple times up to your agreed limit with your lender. This type of debt doesn’t have a set repayment schedule for the full balance, but you normally need to pay a minimum amount every month. For example, with credit cards, you can borrow money every time you put a charge on a credit card. You can only charge your card up to your credit limit and don’t have a set schedule to pay off the full debt.

With this type of debt, credit insurance could be charged as a monthly premium. As a result, each payment is calculated every month either by your average daily balance or your end-of-month balance. Credit insurance would be part of your monthly minimum payment, but the charge would be highlighted separately on your statement.

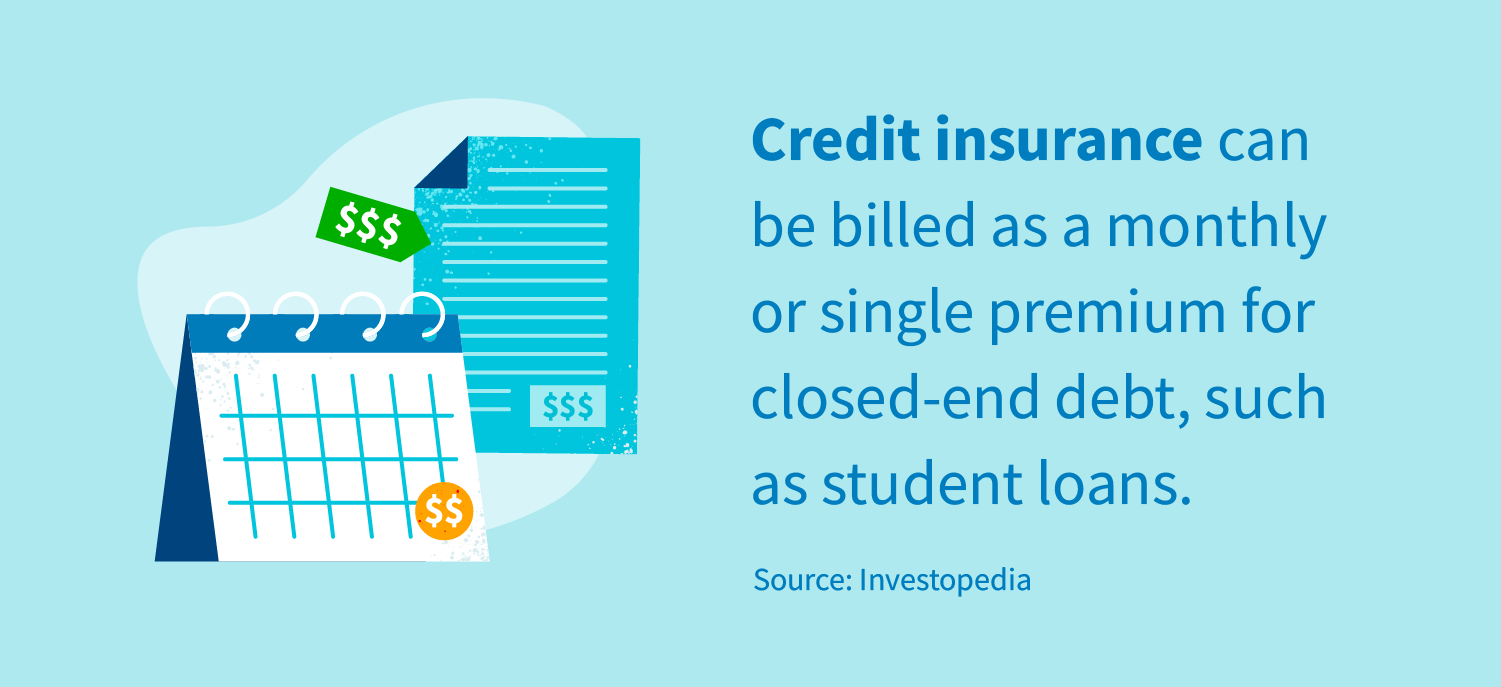

Closed-end debt

This type of debt is repaid during a set time period and paid back on a monthly basis. Student loans are one example of closed-end debt. You pay them back every month and have a deadline to pay off the entire balance.

The cost of credit insurance for this type of debt could be charged as either a single or a monthly premium. Here’s how both options differ:

- Single premium: The cost is solidified at the beginning of the loan and added to the amount originally borrowed. This increases the total sum borrowed and the total interest you’ll pay. This option is for you if you don’t want to worry about paying monthly and want coverage while the loan is out.

- Monthly premium: The cost is calculated by multiplying the premium rate by the outstanding balance on that month’s billing date and added to your monthly payment. This is your ideal choice if you prefer to spread out your payments.

Should you sign up?

Credit insurance could be a good choice for you if it’s affordable and it covers incidents that you don’t already have covered by other policies. Below are some things to consider when exploring your credit insurance options.

When you’re shopping around for policies, think about a few things. Do you already have other insurance that covers you in the event of missed payments? How would a particular credit insurance policy compare to other kinds of coverage?

Once you answer those questions and decide you want to add credit insurance to your plate, it’s time to shop. When you’re evaluating specific policies, run through these questions:

- What is and is not covered by the policy? How much is covered?

- Can the insurance company or lender cancel my insurance?

- Is the lender or insurance company allowed to make changes without letting me know?

- How much does the premium cost and is it financed as part of the loan? If so, how does that impact monthly payments?

- Are monthly payments possible instead of financing the whole premium?

- When is the monthly benefit paid?

- How would my monthly payments differ if I didn’t have credit insurance?

- Can I cancel this insurance? If so, will I receive a refund?

What alternatives are there to credit insurance?

While credit insurance can be a great option for some people, it’s not your only choice when it comes to being financially savvy. Some alternatives to credit insurance include emergency funds, death benefits and better budgeting.

Emergency funds

Instead of taking out an insurance policy that you pay every month, you can instead contribute to a personal emergency fund. You can use this instead of relying on insurance in case you’re in danger of falling behind on payments or coming up short on cash. This way, you can use it for credit-related debt or other surprise costs.

Death benefits

Life insurance pays this benefit to your beneficiary to cover unpaid debts along with additional money for your loved ones. You can consult with your insurance agent if you don’t think your death benefit is enough. If you’re unable to adjust it, then you can begin looking into other life insurance policies and other options.

This route may be cheaper since you can stick to a single policy instead of managing two. You also won’t have to pay interest on your life insurance as you might with credit insurance.

Better budgeting

It may seem obvious, but you may not need credit insurance if you’re confident you can keep up with payments. Smart budgeting and ensuring you don’t spend more than you can handle can minimize the need for credit insurance.

Above all else, make sure you shop around for different policies and weigh the pros and cons before deciding what works for you. It might be more cost-effective to readjust your current budget and spending instead of taking out an additional insurance policy.

Credit insurance is a good idea in the long run if you have a history of late or missed payments. If you’ve had trouble catching up with payments in the past, you should take a look at your credit report first to ensure your current payment history is accurate. If you discover an error, there are options when it comes to disputing it and repairing your credit.