Disclosure regarding our editorial content standards.

You plan on applying for new credit soon—perhaps a mortgage, car loan or credit card—but don’t know where you stand with your credit score. And as much as you want to find out, you’re concerned that checking will negatively impact your score.

So, does checking your credit lower your score? The good news is no, checking your credit report doesn’t harm your credit score. However, you do need to be careful about how often you let lenders check your credit, as that can lower your score.

How do you check your credit report and credit score?

As a consumer, you can check your credit report or credit score in a few ways:

- Many online banks offer a free monthly credit score update.

- Online platforms, such as the three major credit bureaus or other providers like FICO, charge a fee for access to credit reports and credit scores.

- Annualcreditreport.com offers free access to your credit report as well.

The above methods are considered a “soft inquiry” into your credit and won’t impact your credit score.

When applying for new credit, your lender can check your credit report through their own systems. Your credit score won’t be impacted if it’s a soft inquiry. However, lenders usually check your credit as a “hard inquiry,” which lowers your credit score.

What are hard and soft inquiries?

Lenders, creditors, landlords and employers can all check your credit—with your permission. You often have to go through this step to get a new loan, new credit account, rental agreement, auto loan, mortgage and more.

Credit checks are divided into two categories: soft and hard inquiries. Soft inquiries are minimal checks into your credit report—they don’t show all the details of your credit. As a result, a soft inquiry doesn’t affect your credit score. Soft inquiries are noted on your credit report, but they’re only visible to you.

Alternatively, when lenders access your entire credit report, it’s known as a hard inquiry. It’s very common for lenders to use a hard inquiry when you’re applying for new credit so they can vet you as a borrower. Hard inquiries lower your credit score by a few points, but your score typically reestablishes itself from this drop in just a few months.

However, if you have multiple credit applications in a short period, you may find your credit score decreases significantly. Each lender will make a hard inquiry into your credit report, which can lower your credit score and keep it down for a more extended period.

You generally want to space hard inquiries at least six months apart. This means it’s best to avoid applying for several new credit applications too close together or your credit score may suffer.

Why does your credit score fall with several hard inquiries? “Statistically, people with six inquiries or more on their credit reports can be up to eight times more likely to declare bankruptcy than people with no inquiries on their reports,” according to myFico. As a result, it’s likely best to keep the hard inquiries on your credit report to a minimum.

And note that hard inquiries can stay on your credit report for up to two years, during which time the inquiry details are visible to anyone who checks your credit.

What is on your credit report?

Your credit report is full of personal information and relevant financial data of your credit accounts. Generally speaking, your credit report includes four categories of information:

- Personal information: Name, current and former addresses, birth date, Social Security number and phone number

- Credit accounts: The types of accounts, credit limits or loan amounts, dates when accounts were opened and closed, account balances and payment history

- Credit inquiries: The number of hard inquiries into your account

- Public records: Any public records, such as collections, judgments and bankruptcies

Why you should check your credit report

You should check your credit report frequently to make sure there are no inaccuracies that could impact your credit score. Approximately 34 percent of Americans have a mistake on their credit report. These mistakes can keep your score down by several points and cost you financial opportunities.

If you find an error on your credit report, you can file a dispute to have it removed. Or, use the services of credit repair specialists at CreditRepair.com to review your report and file disputes on your behalf.

Does checking your credit report hurt your credit score?

If you check your credit report, it won’t hurt your credit score. However, if you let a lender conduct a hard inquiry into your credit report, your score will temporarily drop a few points—usually for just a few months. Alternatively, if you allow multiple hard inquiries into your credit report in a short time frame, you’ll find your score can decrease significantly and take a while to recover.

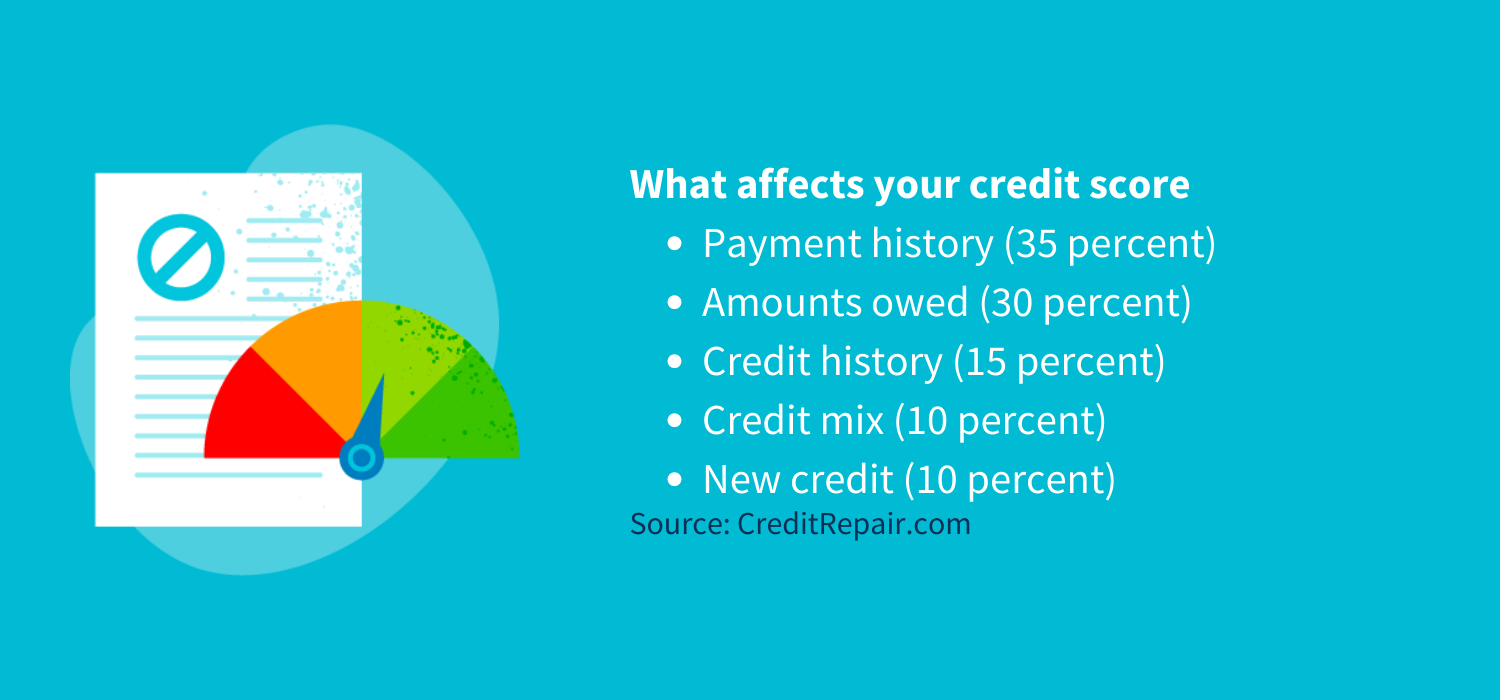

What affects your credit score

So, if checking your credit score doesn’t impact it, you might wonder what does. Your credit score is made up of five major factors, all of which are weighted differently:

- Payment history (35 percent)

- Amounts owed (30 percent)

- Credit history (15 percent)

- Credit mix (10 percent)

- New credit (10 percent)

Understanding these factors can help you avoid mistakes that will negatively impact your score—like closing your oldest credit card or having a high credit utilization ratio.

What is the difference between a credit report and a credit score?

You can think of your credit score as the grade you get for all the details found in your credit report. A credit score is a quick snapshot meant to tell lenders what kind of borrower you are. A higher credit score means you’re a borrower likely to pay your bills on time and in full. A lower score makes you a risky borrower that lenders may only approve with higher interest rates and stricter loan terms.

Often, a credit score on its own isn’t enough information for lenders. Creditors want to know more than your likelihood to pay. They may want to know your outstanding debts or other relevant information. In this case, your credit report is a more detailed account for them to get a complete picture of your financial standing with credit.

How often can you check your credit report and credit score?

You can check your credit report and credit score as frequently as you want. All consumers can receive a free copy of their credit report from each of the three major credit bureaus (Experian, Equifax and TransUnion) every 12 months. If you’d like to review your credit report more frequently, you can pay for monthly access to your account. It can be helpful to check your credit report often so you can quickly spot any inaccuracies and dispute them.

How to check your credit score

Today, most major banks offer free access to credit scores through their online banking platforms. If your bank doesn’t provide this option, you can pay to view your score through an online provider.

If you’d like an overview of your credit, CreditRepair.com offers a free online evaluation that includes your credit score.

How to improve your credit score

Your credit can open the door to many financial opportunities. The good news is that you can always improve your credit by following some simple, healthy financial habits. Increase your credit score by:

- Always paying your bills on time and in full—consider putting bills on auto-pay so you can avoid late payments

- Paying down debts

- Keeping your credit utilization below 30 percent

- Keeping your oldest accounts open to maintain a lengthy credit history

- Having a healthy credit mix of both revolving and installment accounts

- Avoiding too many hard inquiries by leaving at least six months between opening new accounts

And don’t forget to check your credit report frequently. Your report could have inaccurate or false data that keeps your credit score down. The credit repair specialists at CreditRepair.com can take all the work of credit reviews off your hand by evaluating your credit reports and helping you file disputes if needed.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263