Update: As of August 24, 2022, the US government is forgiving student loans debt of up to $10,000 for qualified borrowers. Additionally, President Biden announced additional student loan debt forgiveness of up to $20,000 for qualifying Pell Grant recipients. Federal student loan payments will continue to remain paused through December 31, 2022. Further details will be announced in the coming weeks.

Disclosure regarding our editorial content standards.

Federal student loans have several loan forgiveness programs that borrowers can qualify and apply for. These programs typically have specific requirements and expect payments for many years before qualifying individuals have their remaining balance forgiven. We’re here to explain how student loan forgiveness can affect your credit score and credit report and everything else about student loan forgiveness you should know.

How to know if you qualify for student loan forgiveness

First, it’s important to know that student loan forgiveness programs are only applicable for federal student loans. Unfortunately, if you have a private student loan, you won’t be able to pursue student loan forgiveness.

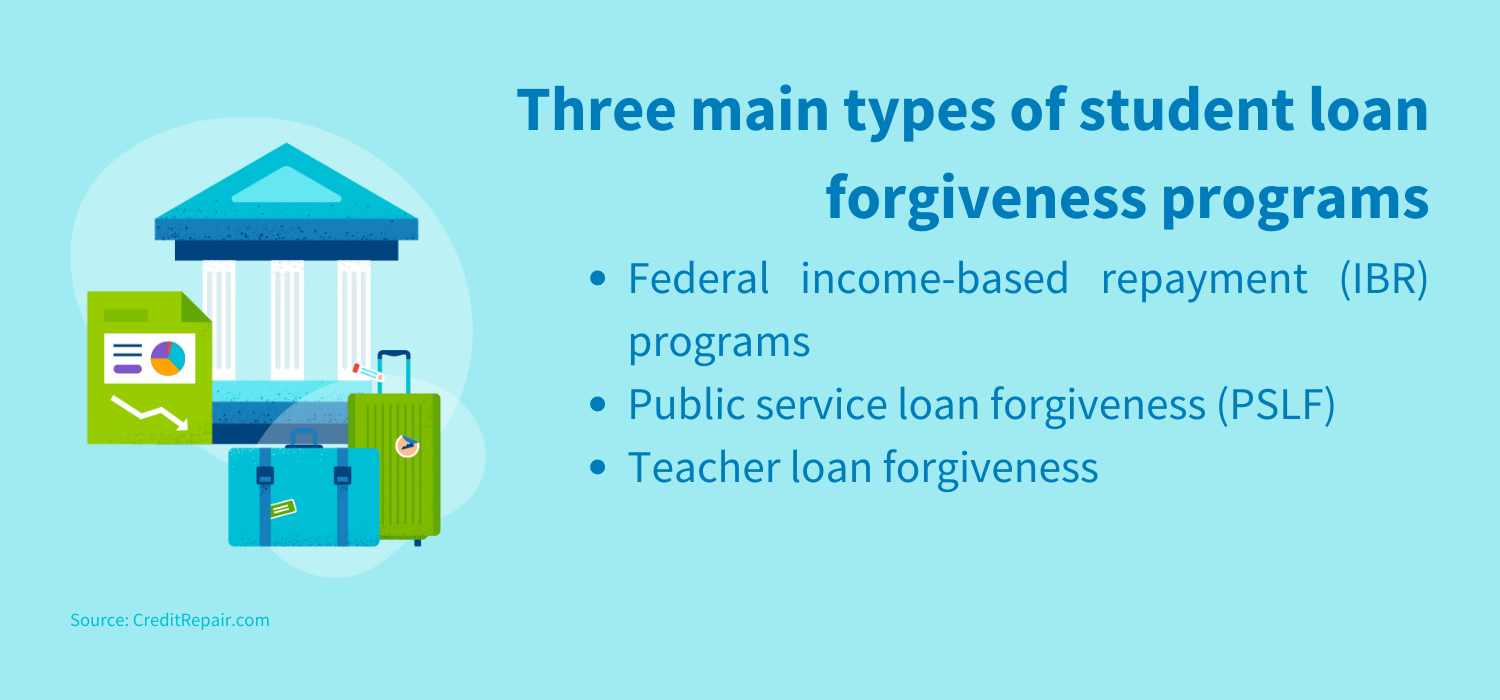

There are three main types of student loan forgiveness programs:

Federal income-based repayment (IBR) programs

Income-based repayment plans are available to all federal student loan borrowers, although the exact repayment details will depend on your financial situation, family size and loan amount. This type of plan looks to make sure that your repayment amount reflects how much you currently make. This helps students afford their student loan payments along with their other living costs.

If you qualify, your monthly payment will be reduced to only account for 10–20 percent of your discretionary income. Additionally, your repayment term will be extended to be a total of 20–25 years. When you complete your repayment term, any remaining balance is automatically forgiven by the Department of Education.

Public service loan forgiveness (PSLF)

The PSLF is designed to help individuals who work for a government agency or nonprofit sector, both of which typically pay much less than the private sector. To qualify for PSLF, borrowers must:

- Get on an income-driven plan for their federal student loan

- Make 120 qualifying monthly federal student loan payments

- Work full time for an eligible nonprofit or a U.S. federal, state, local or tribal government agency

After the 10 years of payments, qualifying individuals will have their remaining balance forgiven. Note that you should do your research into the PSLF if you’re considering pursuing this type of loan forgiveness. Borrowers need to follow specific rules, such as reapplying for PSFL every year.

Teacher loan forgiveness

If you become a teacher after graduating, you may qualify for the teacher loan forgiveness program. High school math and science teachers and special education teachers in all education levels can potentially receive one-time forgiveness of $17,500 on their loans. All other teachers can potentially receive one-time forgiveness of $5,000.

To qualify for teacher loan forgiveness, you must meet the following qualifications:

- Have a direct or federal Stafford loan

- Be employed full time by an elementary school, a secondary school or an educational service agency that serves low-income students for a minimum of five years

- Have a bachelor’s degree and full state certification as a teacher

The teacher loan forgiveness program may not eliminate all your student loans, but even a $5,000 reduction can be meaningful. If you believe you qualify, it may be worth looking into applying.

What to watch out for after forgiveness

So, your loan is forgiven, your debt is at zero and you’re now ready to move on from student loan debt. Before you do this, watch out for these things that may happen to your finances after loan forgiveness:

A refund

Many people receive a refund after their loan discharge completes. You may receive a full or partial refund for recent payments you made.

Negative marks on your credit disappearing

If you have negative marks on your credit associated with your federal student loan—such as a loan default or delinquency—these marks may disappear after your loan is forgiven. There’s no guarantee, but watch your credit report to see if it happens.

Regaining eligibility for federal student aid

To add to the above, if you do see negative marks removed from your credit report, there are additional benefits. A default on your account automatically disqualifies borrowers from receiving new federal student aid. So if the default is removed, you’ll become eligible for federal student aid once again.

Your credit score might dip slightly

Does student loan forgiveness affect credit? Technically, the answer is yes; your credit score may dip slightly at first, but you’ll see it improve quickly.

Your federal student loan is an installment loan. One of the five credit factors that make up your score is credit mix. Your credit score benefits from having diversified credit, such as a combination of installment loans (student loans, mortgages, car loans) and revolving credit (credit cards). Having different kinds of credit makes for a healthy credit mix and shows you can be responsible with various types of credit. If you close your only type of installment loan, your credit will likely see a temporary dip.

The good news is that your score should recover quickly because of your debt-to-income ratio. When you no longer have a monthly payment, the amount of your income going towards debts decreases. This is a positive change that’ll benefit your overall credit.

Your payment history will remain

Note that your payment history from your student loans won’t be wiped out when your loan is forgiven. The payment history from your years of student loan payments will remain. So, if you paid your loans on time and in full, that payment history will continue to benefit you and keep your score high. However, if you had a record of making late or missed payments, these negative marks on your credit report will continue to pull your score down until you build up a positive payment history record.

Your tax burden may increase

Some of the student loan forgiveness programs mark your forgiven debt as taxable income, leading to an expensive tax return. However, the public service and teacher loan forgiveness programs don’t count your canceled debt as taxable income. This is something to consider if you pursue income-based repayment only.

The March 2021 American Rescue Plan did make all loan forgiveness, including PSLF, tax-free until the end of 2025.

The good news is you won’t be left wondering if your canceled loan amount is taxable. After loan forgiveness, you’ll receive Form 1099-C for your taxes, and this cancellation of debt form will show whether the amount forgiven is considered taxable or not.

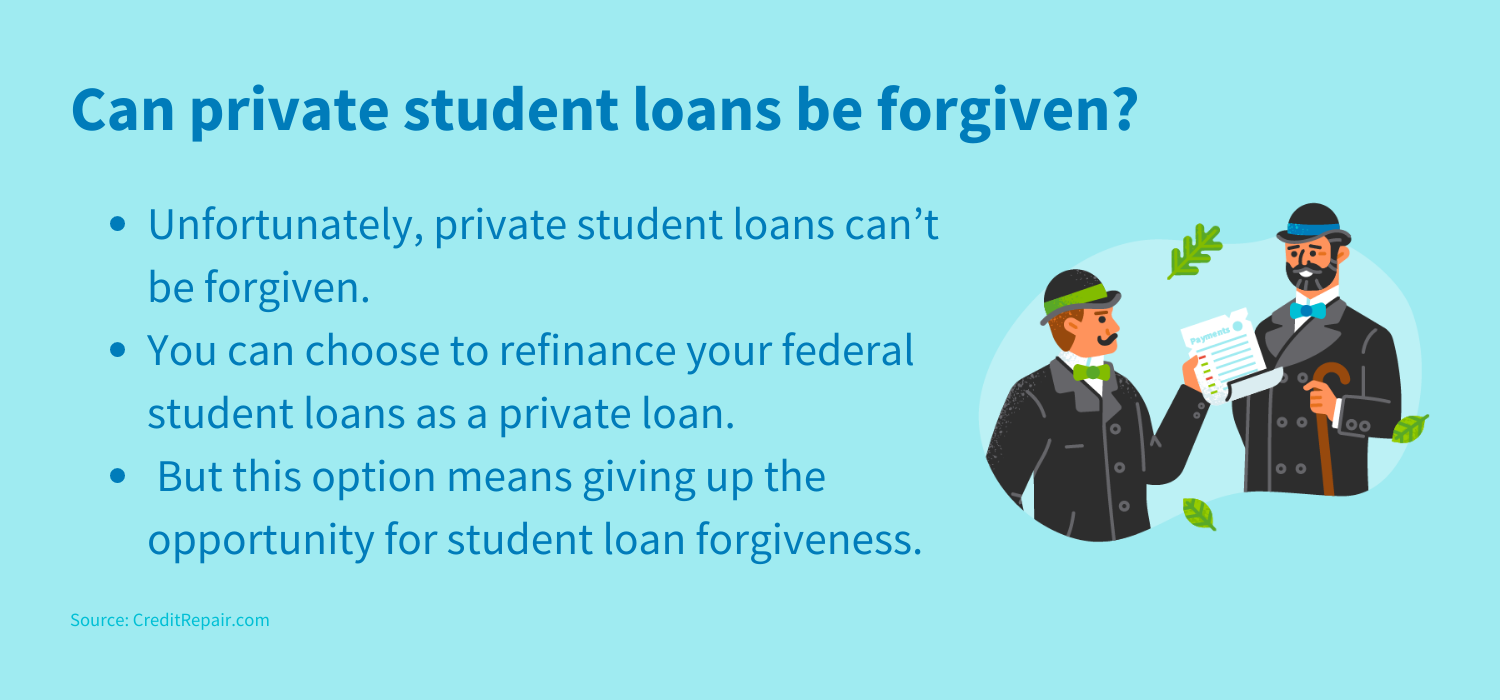

Can private student loans be forgiven?

Unfortunately, private student loans can’t be forgiven. Some private lenders offer borrowers various repayment plan options, including the opportunity to refinance at a lower rate or a longer repayment term.

Many people choose to refinance their federal student loans as a private loan because they can secure a lower interest rate. However, you should carefully consider this decision as it means you’re giving up the opportunity for student loan forgiveness.

If you’re concerned about the impact student loan forgiveness will have on your credit, consider professional credit repair services. CreditRepair.com can help analyze your credit and explain what’s keeping your score down, file disputes on your behalf and help you take back control of your credit health.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263