How medical bills can impact your credit report

Disclosure regarding our editorial content standards.

Even carefully laid financial plans can hit a wall when it comes to medical bills. If that unexpected broken arm or ongoing illness isn’t bad enough on its own, any lingering medical debt could seriously ding your credit report. Talk about adding insult to injury.

Yet for most people, medical bills can be difficult to anticipate and even more difficult to pay off, which means many debts go unpaid and even eventually end up on credit reports. According to the Journal of Internal General Medicine, 137.1 million Americans struggled with medical debt from 2018 to 2019.

How does medical debt work?

After that bleak statistic, is there any good news? Well, the bright side is that medical debts do work a little differently than others. For instance, a doctor or hospital isn’t going to report an outstanding amount to a credit reporting agency right away, which means you may have some time to work out a payment plan or negotiate your bill before it goes to medical collections.

If you still haven’t paid your bill after 90 to 180 days, then it likely would go to a collection agency, according to Equifax. Luckily, starting in July of 2022, medical collection debt won’t appear on your credit report for the first year. That’s great news, but if the debt is still there a year later, it can be hard to keep your unpaid medical debt from affecting your credit score unless you can prove the information is inaccurate. Thankfully, medical debts are also weighed a bit differently depending on which credit scoring model you look at. More recent scoring models tend to soften the impact of medical debts because they’re so common.

If your medical debt is already in collections, know that it won’t be on your credit report forever. After seven years, those debts should drop off. If you’re still worried or have a debt to deal with, we’ve outlined exactly what you can expect your medical bills to do to your credit score, and we’ve provided some steps to help reduce the impact.

Can medical bills affect your credit?

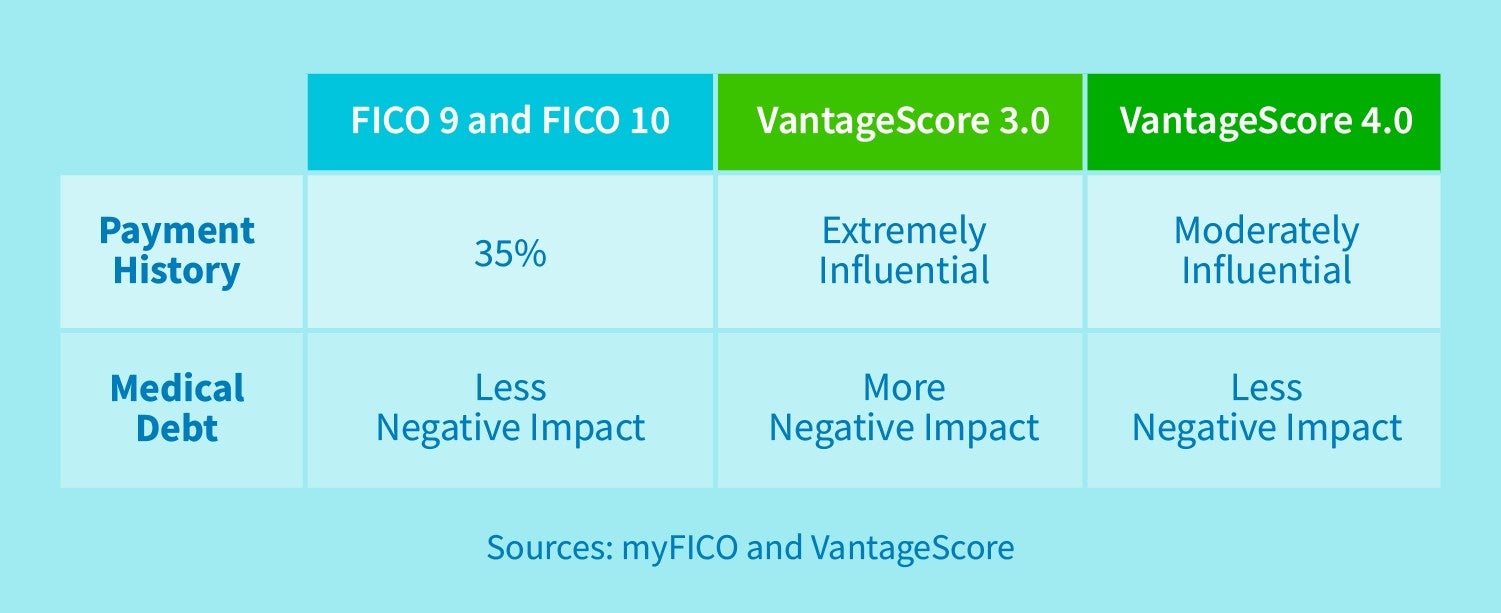

Your payment history makes up 35 percent of your FICO® credit score and a significant part of your VantageScore®. So a medical payment on your credit report can definitely impact your credit score. Even if you had a perfect 800, you could still be in deep trouble after an unpaid medical bill. Yikes.

Don’t panic if your main issue is that insurance takes a while to kick in—since July of 2022, credit bureaus have been required to wait a year before letting any unpaid medical debts affect your credit report. That usually provides enough time for you to work out any disputes with your insurance company.

How much your medical debt affects your credit score also depends on which credit scoring model you look at. The most recent scoring models are FICO 10 and VantageScore 4.0. In both models, unpaid medical debts have less of an impact on your credit score than in past models. Since medical debt is now so common, it’s less indicative of how a borrower will behave with other types of credit.

Depending on the model used, though, your medical debt could have a different impact. For example, FICO 8 is still popular, and it weighs medical debts more heavily. It’s still best to avoid incurring medical debts and keep them from going to collections if at all possible. Once there, it can take years for your credit to improve.

Minimize the impact of medical bills on your credit report

Whether you just opened your first past-due notice or you’ve been receiving collections calls for a while, there are steps you can take to help reduce the negative impact on your credit report, depending on your insurance and the bill’s accuracy. We’ll begin with tips to deal with unexpected medical bills:

1. Know what your insurance covers

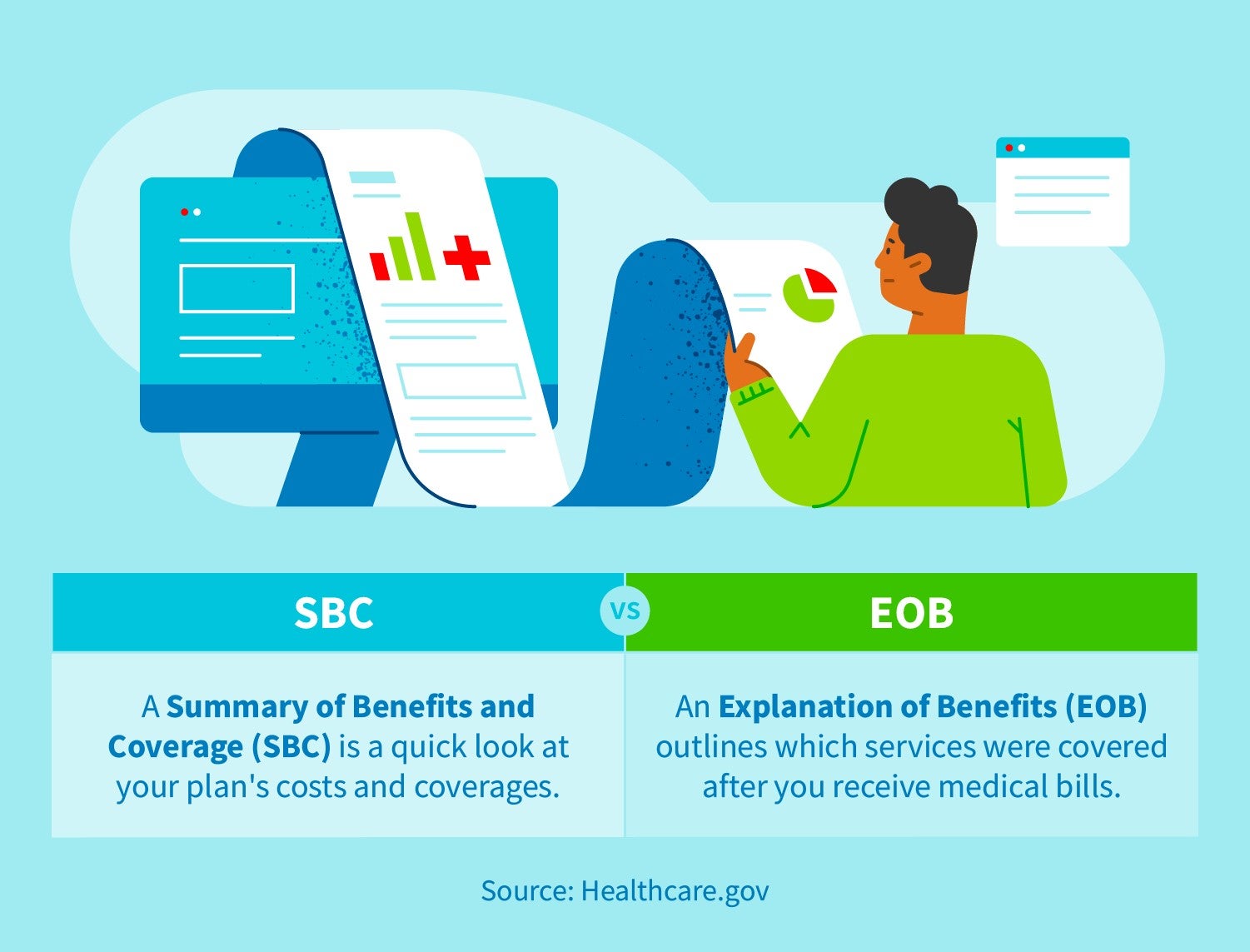

Ideally, you should understand your health insurance coverage before you need to use it. Many services you may have assumed to be covered may not be, so it’s important to know what medical expenses you won’t need to pay, and what you will need to pay. You can find this information in a Summary of Benefits and Coverage, which you can often access online.

After you incur any medical bills, your insurance provider may also send you an Explanation of Benefits statement outlining which services were covered, providing you with the remaining amount to pay. It’s important to carefully compare what was paid for with your benefits and coverage, and contact your insurance provider as soon as possible if you notice any discrepancies. They happen more often than you might think!

2. Determine if you qualify for assistance

Make sure to double check to see if you qualify for financial assistance. Lower-income individuals may qualify for medical bill assistance through programs like Medicaid, local and state programs, religious groups, nonprofits and charities. Additionally, federal law mandates that nonprofit hospitals provide financial assistance programs to qualifying low-income patients. Even though they’re not required to offer these programs, some for-profit hospitals also provide financial assistance.

Even if you aren’t confident you’ll be approved for assistance, the best thing you can do is apply. A hospital may deny your financial assistance application but give you a discount on your bill to help. And a local program or nonprofit may make an exception on your application if you’re close enough to meeting their eligibility requirements.

3. Don’t sweep it under the rug

We get it—seeing several zeros after the amount you owe can be incredibly stressful. However, it’s important not to avoid your bill or put it off until another day. Ignoring it won’t make it go away.

Especially since the communication between healthcare providers and insurance companies can leave room for errors, you don’t want to assume that not hearing anything means you don’t owe anything. After a visit to the doctor, follow up with your insurance provider if you haven’t heard from them in 30 to 45 days to verify you’re caught up on payments.

To understand exactly what you’re being charged for, you can also ask your medical provider to show you an itemized bill. This breaks down everything you’re being charged for all the way down to how many Ibuprofen you were given. It’s much easier to verify charges and reconcile any discrepancies if you understand what you’re being charged for. You may also have more leverage when it comes to negotiating your bills.

And don’t forget, recently the credit bureaus announced that paid medical debt will be dropped from consumers’ medical reports. Meaning even if your bill does go to collections, if you are able to pay it off the debt won’t show up on your credit report. Great news!

4. Negotiate your medical bills

Many people don’t realize they can negotiate their medical bills, but luckily, you can. How much success you find will depend a lot on the particular rules of the care provider or hospital you visited, but it’s usually worth a try.

The Atlantic reports that patients can ask hospitals about financial assistance, or if the bill can be decreased to an amount that they would have charged a Medicare patient. Some hospitals also accept a lower sum if paid in full. Since hospitals often accept much lower sums when selling medical debts to collectors, it is sometimes in their best interest to negotiate with patients before that point.

5. Ask for a payment plan

Another option is to ask your medical provider for a payment plan. These typically involve making several smaller payments over a series of months. If the monthly payments still work out to be too much, don’t be afraid to negotiate further.

It’s important to ask if a payment plan may involve additional fees or interest, and to take that into consideration when choosing your best option. According to MoneyUnder30, it’s not unheard of for large hospitals to offer an interest-free repayment plan for their bills.

Be careful about putting your bill on a credit card to make payments over time. While it can seem like a good short-term solution to keep your debts out of collections, your monthly interest payments can quickly spiral out of control.

There are some medical credit cards specifically designed with no interest options to help you cover deductibles and other expenses up front. However, if you don’t pay within the agreed time frame, you may end up paying interest as well. Carefully consider all of your options before turning to a credit card for help.

6. Consider hiring a medical billing advocate

The last step to consider is hiring a medical billing advocate that will essentially negotiate on your behalf. These professionals contact your insurance and medical providers to help resolve outstanding costs. While you have to pay for this service, it typically pays for itself, as these advocates can secure thousands of dollars off your existing medical bills. Advocates also save you the time and headache of trying to go through the negotiation process yourself.

What to do if your medical debt is already in collections

If your debt is already in collections, take a deep breath. You have options—check out these guidelines to get started.

Verify the charges

When you receive a dreaded collections call, before you make any payments, you should make sure that bill is completely accurate. Don’t assume that a debt collection agency has all the accurate information. According to the Fair Debt Collection Practices Act, you’re entitled to receive the details of your owed debt. If it turns out you’ve been mixed up with another person or you’ve already paid the amount, then you’re off the hook.

After determining there is inaccurate information on your credit report, you may then need to file a dispute with each of the major credit bureaus to get it removed. You will need to contact TransUnion, Equifax and Experian and provide your information and supporting evidence to prove the collection is not yours.

Send a pay for delete letter

Once it's been a year and your debt is on your credit report, that doesn’t mean you’re stuck carrying the mark around for the next seven years. In some cases, you can send what’s known as a pay for delete letter.

This letter is used to get your creditor to agree to contact the credit bureaus to remove the debt from your credit report—as long as you can pay it off. In some cases, you may not even need to pay your full balance. Since creditors typically purchase your debt for a fraction of what is owed, they can still make a profit, even if you pay less than the total amount.

There isn’t always a guarantee that your creditor will agree to do this, however. In some cases, you will need to pay the full amount to convince the creditor to remove the debt from your credit report, and sometimes they won’t agree to remove it.

If you’ve already paid off the amount but still want to have debt removed from your credit report, you can also send a goodwill letter. It’s always worth a try to see if a creditor is willing to work with you.

Understand the statute of limitations

It’s often better to pay your debt when possible, especially since FICO Score 9 and VantageScore 4.0 both disregard paid medical debts. However, if your bill is something you can’t pay, or if it’s from a long time ago, it’s important to understand the statute of limitations on debts.

According to the FTC, the statute of limitations on debts protects consumers from being sued for debts after a certain period of time. The time periods and specific rules vary by state, but it generally ranges from three to six years (you should check the laws in your state). After this time, a debt collector can no longer sue you and force you to pay the debt after it becomes time-barred.

The countdown to when a debt becomes time-barred starts as soon as your first late payment. But here’s the catch—if you make any payments, the clock restarts. This doesn’t mean that you should simply wait out all your debts, though. The statute of limitations doesn’t keep debt from lingering on your credit report for the standard seven years, and paid debts still look better than unpaid ones on your credit report.

A major part of maintaining your overall financial health is staying on top of your credit report. Though unexpected medical expenses can make that difficult, armed with proper knowledge, there are always steps you can take to keep your credit in check.

Related Articles

Maintain your financial health. Stay on top of your credit report.

learn moreFICO and “The score lenders use” are trademarks or registered trademarks of Fair Isaac Corporation in the United States and other countries.

** Your results will vary