Disclosure regarding our editorial content standards.

Most college students can’t afford to work full-time while studying and rely on student loans to fund their degrees. This situation usually means money is tight. And, in addition to having little spending money, students know that their enormous student loans will be due as soon as they graduate. (The average student loan debt as of 2021 is $37,693.)

This is why it’s essential students take advantage of any tax breaks they can. Understanding the common deductions college students can claim can save a person thousands throughout their degree! Luckily, this guide is your one-stop shop for all the tax breaks available to college students.

Credits and deductions: what is the difference?

First, before we get into the exact tax breaks you can take advantage of, let’s define the two main types of tax breaks. As a college student, you can take advantage of tax credits and tax deductions—and these are not the same thing.

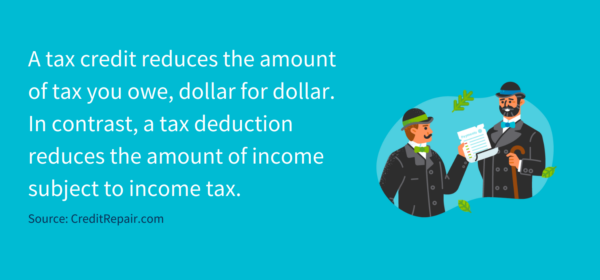

A tax credit reduces the amount of tax you owe, dollar for dollar. For example, if you file your personal taxes and find you owe $2,500, a $500 tax credit would bring your balance to $2,000.

In contrast, a tax deduction reduces the amount of income subject to income tax. So, if you earned $25,000, a tax deduction of $500 would mean you only have to pay income tax on $24,500 of your income.

In general, tax credits are thought to be better than tax deductions because they directly, dollar for dollar, reduce the amount of money you owe. Still, it’s important to remember that tax deductions can also make a big difference in your tax filing. Both tax deductions and credits hold benefits and should be taken advantage of.

College tax credit

There are two major tax credits college students can try to take advantage of:

Lifetime Learning Credit

The Lifetime Learning Credit (LLC) is available to students enrolled in just about any degree or nondegree course. The credit applies to qualified tuition and related expenses paid for eligible students attending qualifying schools. Students don’t have to pursue a degree or attend school at least half-time to qualify.

Eligible students can claim 20 percent of the first $10,000 of their qualified education expenses, to a maximum of $2,000 per tax return.

The LLC is available for an unlimited amount of years, meaning students can claim it every tax year they’ve been enrolled.

There’s an income threshold for this tax credit. Single-income earners making above $69,000 or partners who file together making above $138,000 aren’t eligible for the Lifetime Learning Credit.

Sometimes parents pay for their children’s college fees and take advantage of the tax breaks. If a parent claims a dependent’s LLC, they should understand that the LLC can only be claimed once per household per year. So, if there are two students attending college, the parent can only claim the LLC for one of them.

Lastly, the LLC is nonrefundable. Let’s say your tax liability for the year was $1,400 and you qualified for the entire $2,000 LLC. In this situation, you won’t receive the $600 difference back as a refund.

American Opportunity Tax Credit

The American Opportunity Tax Credit (AOTC) is “a credit for qualified education expenses (tuition, fees and course materials) paid for an eligible student for the first four years of their education,” (IRS) Expenses for housing, transportation, medical care, insurance and nonrequired fees don’t qualify for the AOTC.

College students can get up to $2,500 annually with the AOTC. The credit offers up to 100 percent of the first $2,000 of qualified expenses and 25 percent of the next $2,000. The maximum per annual year is $2,500.

A critical difference between the LLC and the AOTC is the number of years you can claim the credit. If the student takes longer than four years to complete their degree, they’ll no longer be eligible for the AOTC.

Unlike the LLC, the AOTC is partially refundable. Students can get up to 40 percent (or a maximum of $1,000) refunded to them if the credit brings their tax liability to zero.

Additionally, parents can claim an American Opportunity Tax Credit per student in their household.

To qualify for the AOTC, students must be pursuing a degree and enrolled in school at least half-time.

As is the case with the LLC, there’s an income limit to qualify:

- An individual must make less than $80,000, and couples who file jointly must make less than $160,000 to qualify for the full AOTC

- People making over $80,000 but less than $90,000 (over $160,000 and less than $180,000 for joint partners) can still receive the credit but won’t qualify for the maximum $2,500

- Anyone over $90,000 as an individual or $180,000 as a joint pair is ineligible

Claiming dependency: what may be best for your situation

Some parents who continue to financially support their children after they start college consider listing them as dependents. However, deciding whether or not to claim dependency can be tricky and should be evaluated on a case-by-case basis.

First, it’s essential to understand if claiming a college student dependent is even an option in your specific situation. Be aware that the IRS does have specific criteria for which college students can be dependents. The eligibility requirements include details around their age, relationship, financial support and residency.

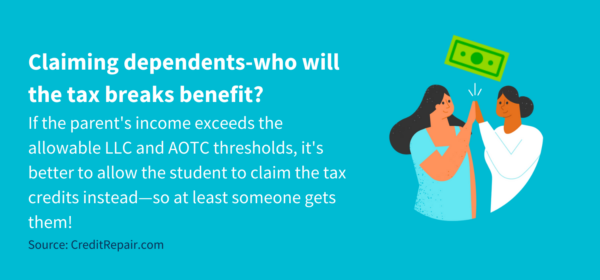

If it’s determined that dependency is an option, the next question is to ask who the tax breaks will benefit more. If the parent pays for the school, they’ll likely want to see some of their money back with these tax credits. However, if the parent’s income exceeds the allowable LLC and AOTC thresholds, it’s better to allow the student to claim the tax credits instead—so at least someone gets them!

College deductions

There are two common deductions college students can claim:

Tuition and fees deduction

As the name implies, the tuition and fees deduction offered an income tax deduction for those paying eligible college expenses. The expenses have to be directly related to education, so items such as household costs, transportation and medical expenses aren’t eligible.

Unfortunately, the tuition and fees deduction expired as of December 31, 2021, and will not be continued going forward. Still, individuals who paid qualified tuition and fees from 2018-2020 and didn’t claim this deduction already can still do so. The maximum amount an individual can claim is $4,000 to reduce their taxable income.

As this is a tax deduction and not a credit, individuals will not receive any money back if their tax liability is brought down to zero.

The tuition and fees deduction has an income threshold of $80,000 or less for individual earners and $160,000 or less for those who file taxes jointly.

Student loan interest tax deduction

While it may be a bit of a disappointment that the tuition and fees deduction has been canceled, the good news is that the student loan interest tax deduction still applies. Anyone paying for interest on their student loans can deduct up to $2,500 in interest fees annually. This applies to both interest on mandatory payments and interest paid on bonus payments, all up to a maximum of $2,500 in deductions combined.

This deduction only applies to qualifying student loans, so private loans from friends, family and workplaces aren’t eligible.

To qualify for this tax deduction, the individual must have paid interest on a qualified student loan in the previous tax year. Additionally, single filers must make an income of less than $85,000 (as of 2021) and joint filers must earn less than $170,000 to be eligible for the student loan interest tax deduction. This income threshold is set annually and can potentially change every year, so it’s important to do your research.

Tax-free college payment accounts, bonds and programs

Tax credits and deductions aren’t the only place for savings as a college student. Individuals can use a 529 or Coverdell Education savings account to keep their college savings. These accounts allow for tax-free withdrawals and tax-free earnings growth, which can save hundreds or thousands of dollars. Some states even offer programs that give you tax benefits when you contribute to these accounts.

- A 529 account allows you to enroll in a prepaid tuition plan, so you lock in current tuition rates. Alternatively, you can use a 529 account as a savings account where your money can grow tax-free.

- A Coverdell Education savings account allows you to save and withdraw money tax-free as long as it’s used to pay for education.

Additionally, you can explore the idea of investing in an education savings bond program. These programs allow individuals to invest in savings bonds that are tax-free when they’re cashed out as long as they’re used to pay for higher education.

Lastly, students can consider taking advantage of student credit cards, which often come with low or no fees and perks such as gift cards, cash back and travel points.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263