How to rebuild your credit: 11 tips for 2023

Disclosure regarding our editorial content standards.

Rebuilding your credit can feel a lot like building a house with no instructions. With dozens of moving parts, this can be a confusing process that you may feel like you need a hard hat to conquer. However, learning how to rebuild your credit is a lot more like assembling a piece of furniture—you just need the right directions and tools.

It begins with examining your credit report for any discrepancies, and if you find information that’s inaccurate, unfair or unsubstantiated, your next step is to submit letters of dispute.

Once you do this, it takes roughly three to six months to resolve general disputes—this time span depends on the amount and types of negative marks you have to address. You need to know what to look for, what steps to take and who to contact to fix errors.

To simplify the process of rebuilding your credit, we’ve outlined the main factors and strategies to learn how to rebuild successfully. This way, you have all the tools and directions you need to set you up for success to fix your credit.

11 steps to help rebuild your credit score

Depending on your present situation, there are dozens of techniques that can be implemented to rebuild your credit score. While there isn’t a one-size-fits-all approach or a single step to make your financial headache disappear, combining multiple strategies can help ease the pain and get you on the path to fixing your credit score.

Table of contents:

- Understand what factors affect your credit score

- Review your report and statements

- Pay down open or delinquent accounts

- Pay on time

- Don’t cancel your credit cards

- Get a secured credit card

- Get a cosigner

- Open a joint credit card account

- Consider credit counseling

- Create a budget and an emergency fund

- Think twice about opening new lines of credit

- How long does it take to rebuild credit?

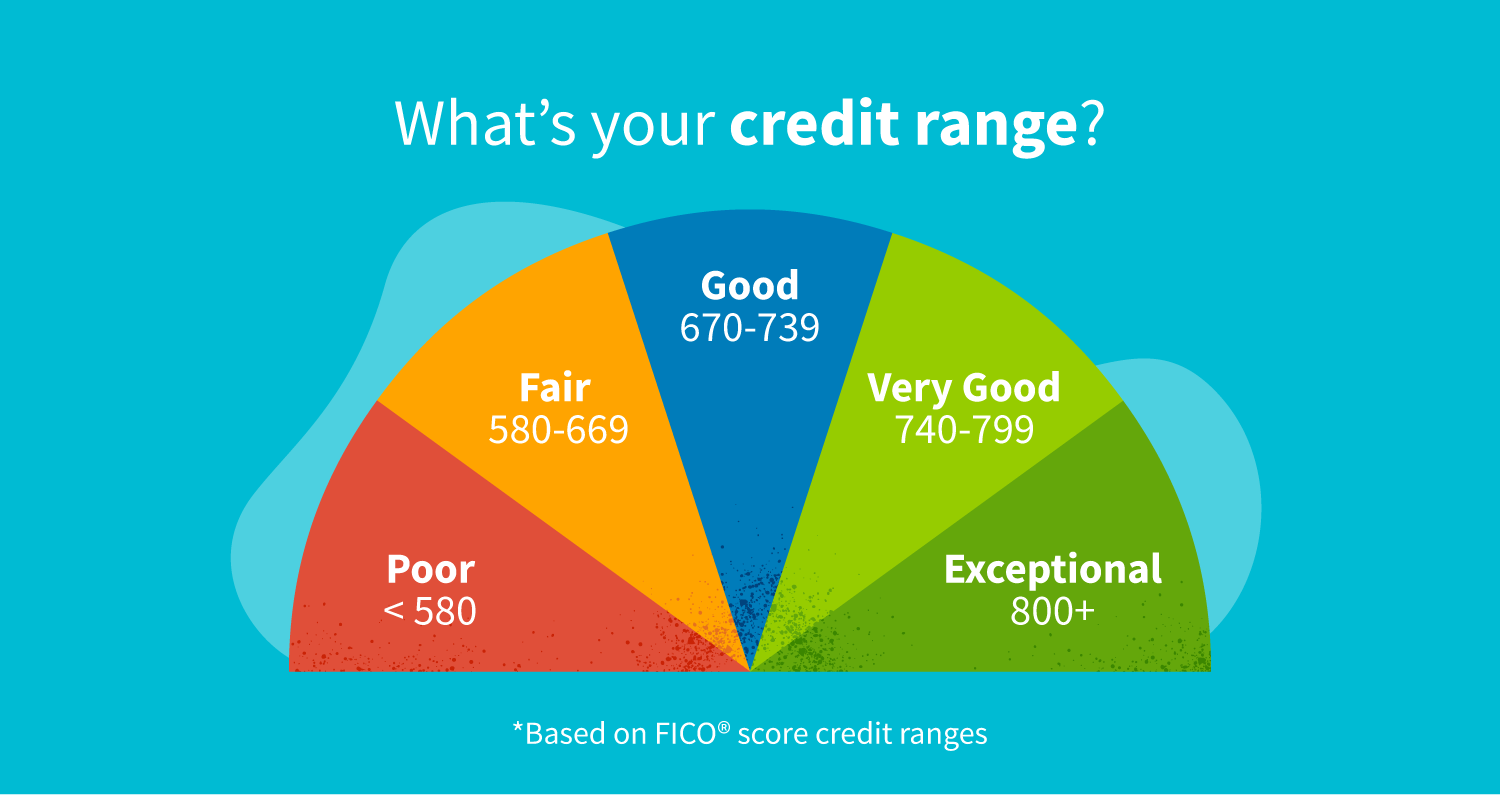

1. Understand what factors affect your credit score

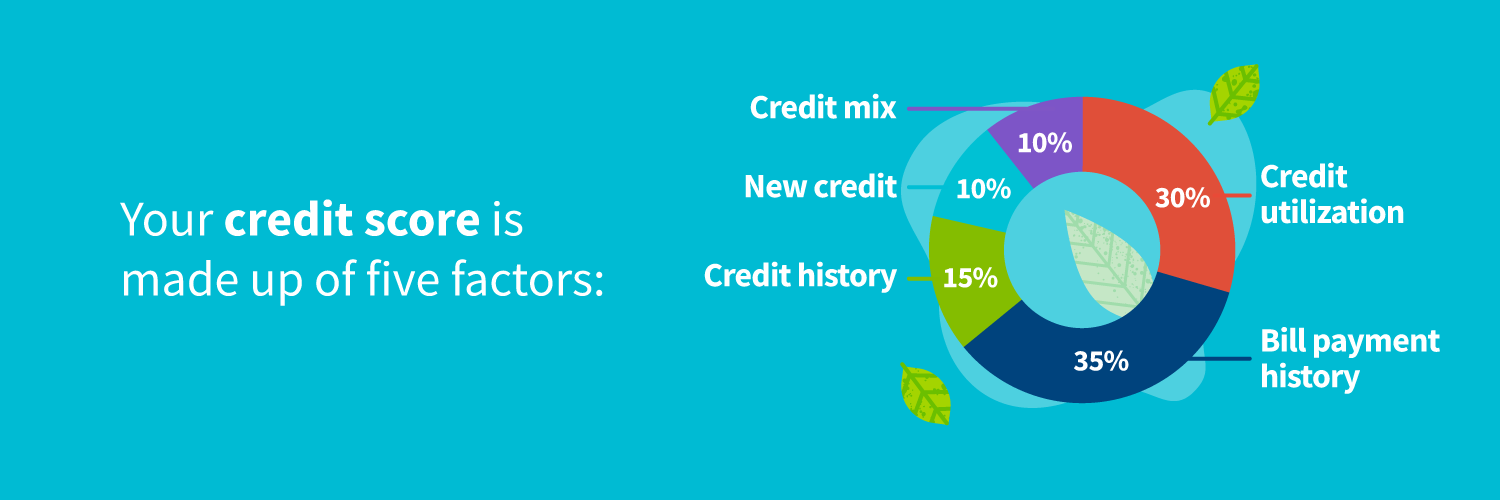

The first place to begin when rebuilding your credit score is examining your credit report. There’s a lot of information on your credit report, and each factor impacts your score differently. The following five factors from your credit reports are used to calculate credit scores:

- Bill payment history: 35 percent of total FICO score. Outlines if bill payments were received on time or late. Past-due payments stay on your credit report for up to seven years.

- Credit utilization: 30 percent of FICO credit score. A calculation of the total amount owed, compared to the credit limit. Utilization fluctuates based on the payments made every month.

- Credit history: 15 percent of FICO credit score. The average of how long all your accounts have been open.

- Credit mix: 10 percent of total FICO score. The types of credit accounts you’re using. This includes credit cards, loans, collections and other accounts.

- New credit: 10 percent of FICO credit score. The number of hard inquiries (e.g., recent applications for new credit and loans) that appear on your credit report.

Now that you know how your score is calculated, you can focus on finding which factors are hurting you the most—late payments? Accounts in collections? Once you’re able to identify your major pain points, you can begin coming up with a plan to raise your low credit score.

2. Review your report and statement for errors

It’s important to regularly take the time to check your credit score and credit accounts for unusual activity and signs of identity theft. Unusual activity can include new accounts you didn’t open or purchases on your statement you didn’t make.

Mark off your calendar and take an hour each month to review your statements. The sooner you alert your creditor via a dispute letter, the easier it will be to address this issue.

If you discover that someone’s stolen your identity, you should:

- Freeze your credit

- Alert your bank and activate fraud alerts

- File a claim with your identity theft insurance provider

- File a report with the Federal Trade Commission

- Alert your local police department

To protect yourself from identity theft:

- Use a credit monitoring service

- Choose strong passwords for all online accounts

- Use a different password for each account and change them often

- Shred any mail or old credit cards that contain personal information before throwing them away

- Use virus protection on your computer

3. Pay down open or delinquent accounts

If you have any credit cards that are gathering dust or have an account in collections, you’ll want to focus on paying down these accounts first. Even if you haven’t used a credit card in a while, it might still carry a balance—and it will accrue interest until you pay it off.

Defaulted accounts will also hurt your credit score, but the amount due generally doesn’t change if a payment is missed. A defaulted account can be paid down in small, consistent increments over time.

If you have debt on multiple accounts, it can be overwhelming to figure out which to prioritize. If you can, pay at least a little more than the minimum on each account.

You can keep a spreadsheet to keep track of this on a monthly basis, or consider credit counseling for expert advice to reduce your debt.

4. Pay on time (avoid late payments)

Remember, late payments are a part of your credit history, and they account for 35 percent of your credit. This is the largest part of your score, so it’s important to always make your minimum payments.

Credit card issuers and other creditors will charge a penalty fee (usually between $29 and $40) on top of the initial payment due when you miss a payment. This makes getting caught up and paying off the account more challenging, especially if you’ve been late on payment more than once.

When you miss a payment:

- After 30 days: the negative mark appears on your credit report.

- After 60 days: your interest rate will increase if your issuer has a penalty interest rate as part of your credit card terms.

Lenders can keep the increased rate in place for as long as their terms state, sometimes as long as six months, before reviewing your account. Even if the rate is lowered, the damage is already done. Late payments can stay on your report for up to seven years.

If on-time bill payment is something that you struggle with, one option is to set up automatic payments for your monthly expenses. They’re on the same day every month, which means you only need to focus on having money in your bank account instead of paying on time.

5. Don’t cancel your credit cards

You’ve probably wondered if closing a credit card affects your score—the answer is often yes. It seems counterintuitive to keep a line of credit open once you’ve spent months paying it off, but keeping it open has a lot of benefits, even if you aren’t using it.

Remember your credit utilization ratio, accounting for 30 percent of your credit score? Closing a credit card can cause your ratio to increase and limit your ability to make large purchases. Additionally, closing a credit card can shorten your credit history because it shortens your average credit account age. To lenders, this can look like you haven’t been building your score for very long (even if the opposite is true).

Generally, lenders like to see a combination of personal loans and good-standing credit accounts on your credit report. Getting rid of credit cards gives you less leverage. Plus, these cards can be used as a backup if emergency funds run low.

6. Get a secured credit card

If you’re having difficulty qualifying for a traditional credit card, consider a secured credit card. With a secured credit card, your credit limit depends on your security deposit—so you can only spend the amount you deposit (typically between $200 and $5,000). Issuers generally approve a wider range of borrowers for these types of cards because the cards are secured with initial funds.

If you’ve signed up for a secured credit card, be sure to make regular, on-time payments on the card. While it’s easier to get a secured card if you need to rebuild credit, it comes with the same consequences as a traditional card if you can’t make your payments.

7. Get a cosigner

Another option that can help you qualify for a credit card is having a cosigner. Gaining the assistance of a cosigner is best for people with low credit scores or those who don’t make enough money on their own. A cosigner will be responsible for your payments if you don’t make them yourself, so lenders are more likely to approve you if you have cosigner.

Once you are approved, the new account will show up on both of your credit reports. Heads up: cosigning consequences can be severe for missed payments because both individuals’ scores will be affected. This can damage both credit scores and the relationship, so consider this option carefully, and be sure to ask someone you trust to be a cosigner (like a parent, guardian, sibling or close relative).

If you have difficulty managing your credit payments or you struggle with overspending, opening a new credit card isn’t always the best idea. Building healthier credit habits on your existing cards might be a better option if you struggle with debt.

8. Open a joint credit card account

Opening a joint credit card account is a lot like having a cosigner. If you have bad credit, opening a joint account with someone with good credit gives you access to better interest rates, lines of credit and other benefits you wouldn’t have access to on your own.

However, there are consequences to having a joint account, just like with cosigning. If you miss payments or submit them late, then both you and the joint account owner will take a hit on your credit reports.

So, before taking this route, have a conversation about expectations with the other joint account owner. Strategize the best options for proceeding once the person building credit—whether you or the other account owner—gets back on their feet.

9. Consider credit counseling

Pursuing credit counseling is an excellent option that shows you’re determined to improve your credit. The National Foundation for Credit Counseling (NFCC) is a nonprofit agency that advises clients on financial solutions for paying off debts.

These agencies examine your credit report and implement a debt management plan (DMP) and consolidation options to help you organize expenses and lower payments. If you’ve exhausted your other credit-building options or just don’t know where to start when it comes to rebuilding your credit, credit counseling may be a good step for you to consider.

10. Create a budget and an emergency fund

Trying to save money while paying off debt is challenging, but there are many benefits to having an emergency fund set aside. Having reserved emergency funds will prevent you from relying on credit cards, and when miscellaneous incidents occur, such as car repairs or an unexpected medical bill, you’ll have cash on hand.

If you struggle with budgeting, you have several options to help you track and reel in your spending. There are various financial apps that can help track your monthly bills and savings, so you can easily see any areas of spending you should cut back on.

11. Think twice about opening new lines of credit

When opening a new line of credit, your lender will usually conduct a hard inquiry check into your credit. A hard inquiry can lower your credit score by a few points, but your credit score should recover from this slight dip in a few months.

However, if you open several lines of credit in a short period, you’ll have multiple hard inquiries on your credit report. Numerous hard inquiries in a short span can harm your credit score significantly.

Generally speaking, it’s best to wait six months between new credit applications, so you don’t have multiple hard inquiries in a row. As you’re currently rebuilding your credit, avoiding new credit avoids additional hard inquiries, which is beneficial to your credit score.

This doesn’t mean you should never open a new line of credit when you’re trying to rebuild your credit. In some cases, it’s necessary to help lower your utilization rate. Just be careful about overusing a new line of credit and worsening debt.

How long does it take to rebuild your credit?

Every credit situation is different, so everyone can expect a different timeline for how long it will take to rebuild their credit. Depending on the severity of past mistakes (like bankruptcy), it can potentially take a long time to make a full recovery. Here’s how long negative information stays on your credit report if it doesn’t need to be disputed:

- Chapter 7 bankruptcy (completely removes debt): Stays on credit reports 10 years after filing date

- Chapter 13 bankruptcy (debt is repaid under pre-negotiated terms): Remains on credit reports seven years after original filing date

- Collection accounts: Stay on credit report for seven years after the original delinquency date

- Hard inquiries: Reflected on credit report for two years, with impact on credit score lessening over time

- Late payments: Stay on credit reports seven years after the account is first brought current from delinquency—if a missed payment goes to collections, the derogatory mark will last seven years from the date of the original missed payment

This may seem like a long time to rebuild your credit, but there are steps you can take immediately to begin rebuilding while you wait for the more official processes to take effect:

- Organize your debts smallest to largest to decide which to prioritize.

- Starting with smaller debts, dispute each inaccuracy on your credit report individually with the credit bureaus or your creditors.

- The credit bureau has 30 to 45 days to contact creditors, verify the information and respond to your dispute. Cases can take longer for more complex situations, such as Chapter 13 bankruptcy.

It might seem counterintuitive to begin with smaller debts, but this strategy, known as the snowball method, can help you rebuild your confidence as you chip away at your debt.

This can help put you in the proper mindset to start rebuilding your credit. It takes organization and discipline to repair credit. Most importantly, be patient with yourself. It’s likely that you didn’t get bad credit overnight, so know that you likewise won’t get good credit in a day (unfortunately).

Look for debt and credit solutions, stay consistent with payments and keep making smart personal finance choices. You’ll see inaccurate negative information disappear from your credit report over time.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

If you need help, call the credit experts

learn moreFICO and “The score lenders use” are trademarks or registered trademarks of Fair Isaac Corporation in the United States and other countries.

** Your results will vary