Disclosure regarding our editorial content standards.

The CFPB annual report is a document summarizing all the complaint responses the Consumer Financial Protection Bureau receives from three national credit reporting agencies (NCRAs)—Equifax, Experian and TransUnion—each year. This important because it provides an overview of the most common consumer complaints and makes it easier to identify trends.

The CFPB is a government agency tasked with protecting consumers from unfair or deceptive practices in the financial industry as well as helping consumers understand the financial marketplace. This year’s report focuses on how NCRAs have recently failed to respond to consumer disputes in alarming numbers. This matters because inaccurate items on credit reports can have very negative consequences for those affected.

Read on to learn more about what disputes are, why a dispute may not be resolved successfully and what options you have if you need to remove inaccurate items from your credit report.

What are disputes and why are consumers making them?

When consumers find incorrect information on their credit reports, they can file a dispute with the three major credit reporting agencies to potentially get the information taken off of or modified in their credit reports. This can often have a positive effect on a consumer’s credit score.

The Fair Credit Reporting Act (FCRA) requires each NCRA to conduct a “reasonable investigation” if a consumer disputes the accuracy or completeness of the information in their credit file. Below are just a few examples of inaccurate information that may appear in a credit report:

- Closed accounts reported as open

- On-time accounts reported as late

- Incorrect account balances

- Incorrect credit limits

- The same debts listed more than once

Consumers also file complaints when NCRAs don’t remove outdated negative information as required. For example, some items are supposed to be removed after seven years, including late payments. If a late payment is still on a consumer’s credit report after 10 years, the consumer might file a dispute with the NCRAs.

How are the disputes being handled?

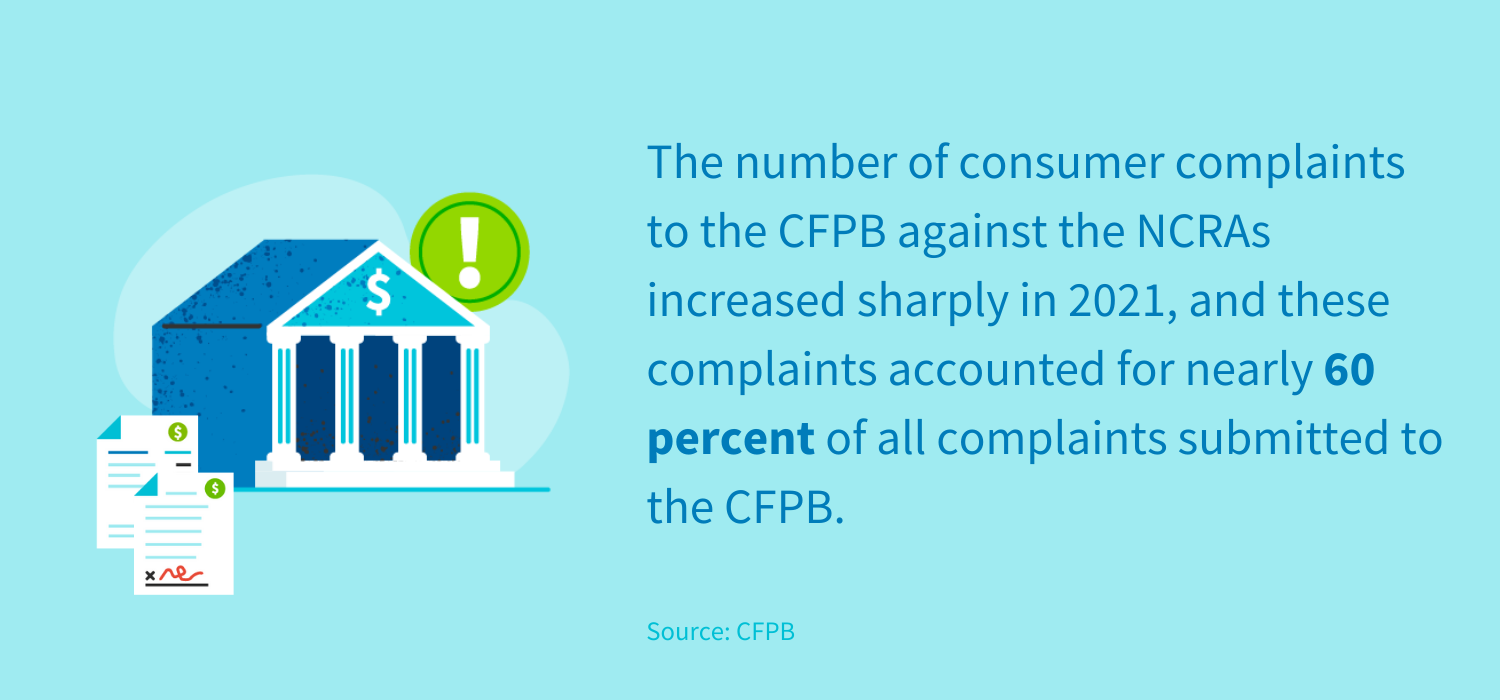

The disputes are in many cases not being handled well. According to the CFPB annual report, the NCRAs are not responding to consumers’ disputes or addressing the incorrect information on many consumers’ credit reports. The number of consumer complaints to the CFPB against the NCRAs increased sharply in 2021, and these complaints accounted for nearly 60 percent of all complaints submitted to the CFPB.

Why disputes may not get addressed

Many consumers—in excess of 70,000—reported that their disputes with the NCRAs aren’t being addressed in a timely manner. Here are a few reasons this might be the case:

1. Heavy workload

The FACT Act, FCRA and Dodd-Frank Act are all designed to protect consumers, but it takes a lot of time, energy and money for the NCRAs to comply with these laws. In some cases, disputes aren’t addressed in a timely manner because an NCRA doesn’t have enough staff to review complaints or update consumer information in their systems. Staff may also be busy answering telephone calls or performing other duties, leaving them less time for responding to CFPB complaints.

2. Automated system glitches

Another reason disputes aren’t addressed in a timely fashion is because automated systems can be faulty. We rely on technology for almost everything, but it doesn’t always work perfectly. Employees of an NCRA may have trouble accessing disputes or may not be able to respond due to network connectivity issues or problems loading disputes in their systems.

3. Difficulty communicating with data furnishers

NCRAs rely on data furnishers—the credit card companies, banks and other financial firms responsible for reporting account information—to respond to their queries quickly. For example, if a consumer files a dispute stating that an NCRA is reporting a late payment on an account that’s never been late, the NCRA must contact the data furnisher and ask for more information.

If the data furnisher doesn’t respond in a timely manner, the NCRA can’t respond to the complaint effectively. Additionally, the NCRAs receive data from more than 10,000 data furnishers, resulting in a significant amount of back-and-forth communication.

4. Disputes submitted by representatives

The CFPB report also found that NCRAs are not responding properly to disputes submitted by consumer representatives. Instead, NCRAs are allowed to respond via an administrative process.

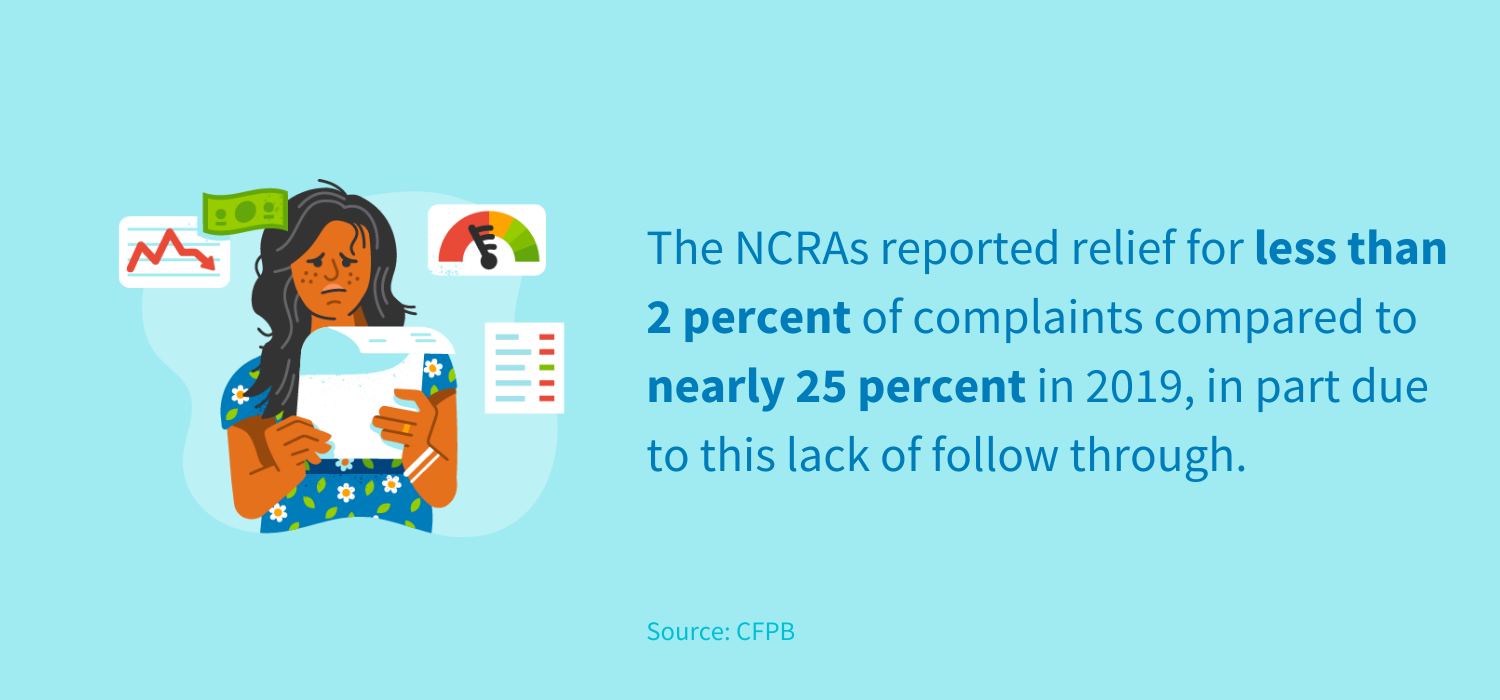

This process doesn’t require an NCRA to provide a substantive response to the consumer. The NCRAs reported relief for less than 2 percent of complaints compared to nearly 25 percent in 2019, in part due to this lack of follow through.

How can you address incorrect items on your credit report?

The CFPB is a helpful agency, but filing a complaint with the CFPB is only one way to address incorrect items on your credit report. Instead, consider these options:

File disputes with the NCRAs yourself

You can file a dispute with the NCRAs yourself, if you prefer. You can file a report online, though sending your dispute via certified mail creates a paper trail, making it easier to prove the NCRA received it.

Your dispute letter should describe the error and explain why it’s incomplete or inaccurate. It’s also best to include supporting documentation. For example, if a credit card company is reporting that you have a $2,500 balance on an account that has a $0 balance, you may want to provide a copy of your most recent statement showing that you don’t owe the company any money.

Work with a credit repair company

The dispute process can be stressful, especially if you’re dealing with identity theft and have to file multiple disputes with all three NCRAs. Fortunately, you don’t have to go it alone. CreditRepair.com can help you file detailed disputes and follow up if the NCRA doesn’t respond as required.

It’s important to dispute inaccurate information right away, as negative items lower your credit score and may make it difficult to qualify for new accounts. Even if you do qualify, you may have to pay a higher interest rate, making it more expensive to open a credit card, take out a home loan or purchase a vehicle. See if CreditRepair.com can help you fix your credit, giving you access to more sources of financing and making it easier to qualify for favorable credit terms.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263