Disclosure regarding our editorial content standards.

Applying for a mortgage is a little different from applying for any other type of loan. Because of the size of the loan, you’ll undergo a much more thorough underwriting process for a mortgage than you would for an auto loan, a student loan, or most personal loans.

One thing your lender will do is examine your tri-merge credit report.

What is a tri-merge credit report?

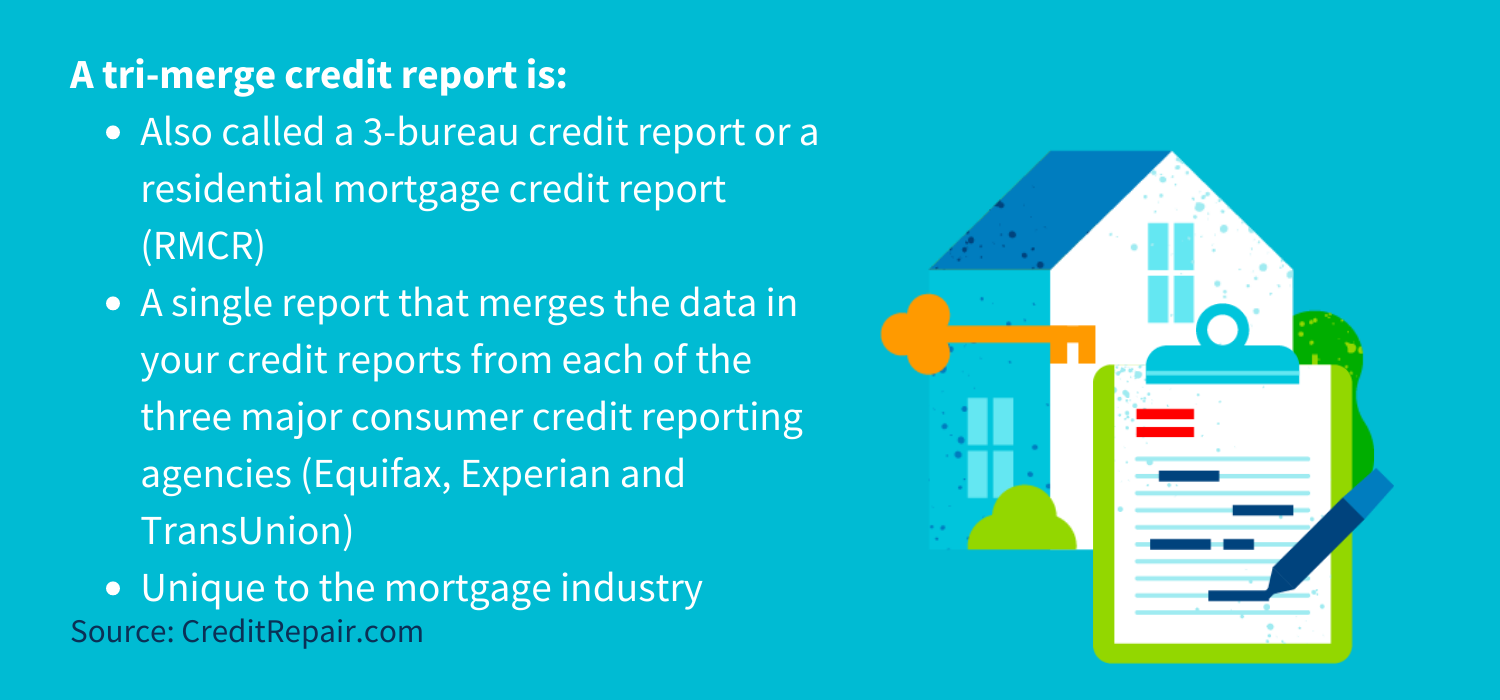

A tri-merge credit report is:

- Also called a 3-bureau credit report or a residential mortgage credit report (RMCR)

- A single report that merges the data in your credit reports from each of the three major consumer credit reporting agencies (Equifax, Experian and TransUnion)

- Unique to the mortgage industry

When you apply for a credit card, the card issuer will pull one of your credit reports, but is very unlikely to examine more than one. There are probably exceptions, of course. Credit card issuers generally have relationships with all three credit bureaus, and there’s no way to know ahead of time which credit report will be pulled when you apply.

A mortgage lender, on the other hand, will purchase a special credit report that includes all of the credit data available on you from all three credit bureaus. If you apply with another person, like a spouse, the lender will purchase that same special credit report on him or her as well.

What does a tri-merge credit report include?

A tri-merge credit report includes your credit information from all three credit bureaus, which are Experian®, Equifax® and TransUnion®. The report merges your data, such as payment history, loan accounts, inquiries, disputes, credit utilization and credit card accounts. They show how much is owed on your loans and if any late payments were made within the past seven years.

Other financial information a tri-merge credit report contains includes bankruptcy filings made within the past seven to 10 years or foreclosures from the past seven years.

Is there a tri-merge credit score?

Credit scores are not merged. When a mortgage lender pulls your tri-merge credit report, it will include your FICO® score as calculated by each credit reporting agency.

What credit score does a mortgage lender use? Most lenders use the middle score (or the lower middle score if you jointly apply).

Also, remember that the credit score a mortgage lender sees can be quite different from the free or purchased credit score you get online. A consumer credit score may give you a good idea of where your credit stands, but a mortgage credit score is tailored to mortgage risk factors.

Why do mortgage lenders get a special credit report?

Most U.S. consumers have credit files with each of the major credit reporting agencies (and credit files with other lesser known credit reporting agencies, too). The reports do not match exactly, however. Reporting to credit bureaus is voluntary. Creditors are not obligated to do it. Furthermore, they don’t have to report to all three bureaus. The data in your file can vary from one report to the next.

Mortgage lenders have a special interest in examining all of your credit data in order to make the best possible decision when it comes to offering what probably amounts to the biggest loan you’ve ever taken. They need to assess your creditworthiness as accurately as possible, partly to protect their own interests and partly to be sure the loan complies with the many laws and regulations that govern mortgages.

The tri-merge credit report allows mortgage lenders to see a complete picture of how you have used credit in the past.

Does a tri-merge credit report help my mortgage application?

A tri-merge credit report is just as likely to help or hurt your mortgage application as any of your reports individually. Of course, if one of your reports has more negative items than the others, you may have wanted a different report pulled for your mortgage application, but the lender likely won’t change their processes because of your preferences.

Each lender has its own set of credit requirements for borrowers who want to buy a house. They’ll check your tri-merge credit report to see how responsibly you manage your credit and whether you have a history of making payments on time. This information, along with your FICO® credit score, will be used in the lender’s evaluation of your mortgage application.

A high credit score and clean report can help you qualify for mortgage loans with lower interest rates. If your report contains higher balances and payment inconsistencies, you may still qualify for the loan but may have to pay a higher interest rate.

Where does a tri-merge credit report come from?

The major credit bureaus sell tri-merge credit reports, and so does a whole industry of other providers called mortgage reporting companies. Whatever the source, the report combines the data found in the three one-bureau credit reports to eliminate duplicate entries. The combined credit report is much easier to read and evaluate than three separate reports.

Where can you get a tri-merge credit report?

You may have a hard time getting your hands on a copy of your tri-merge credit report. Generally, mortgage credit reporting companies only sell them to lenders.

If you have applied for a mortgage, you can ask the loan officer to provide you with a copy of your report. If that person cannot provide it, the company that prepared it for the lender may be able to. There is no law, however, that entitles you to a copy, for free or otherwise, unless your application is denied.

Any time your application for credit is denied, you are entitled by law to a copy of the credit report the denial was based on. This copy may not include your FICO® scores.

If you are able to get a copy of your tri-merge credit report, it should include your FICO® score from each bureau.

Where can you see your tri-merge credit report?

A tri-merge credit report doesn’t have any information that doesn’t already appear on your credit reports from Equifax, Experian and TransUnion.

The law says you can request a free annual credit report from each of major credit reporting agency, and they must provide it to you so long as they can verify your identity. Do this by visiting AnnualCreditReport.com, which is the only official website authorized to provide you with those free copies. You don’t have to request them all at once. You can stagger them throughout the year if you prefer.

If you want to apply for a mortgage in the future, you don’t need to see a tri-merge credit report in order to know what’s in your credit reports.

Tri-merge credit reports are generally sold to mortgage professionals. If you’re curious about what shows up on the report, ask your loan officer for a copy of the report when applying for a mortgage loan. You can also sign up for a 3-in-1 credit monitoring service. This won’t produce a tri-merge report, but you will get access to reports from each of the three major credit bureaus.

Can you order your tri-merge credit report?

No, this report is usually only offered to lenders and can’t be ordered by an individual. However, you can order individual copies of your credit report from each of the three bureaus.

Repair your credit

If you are looking to apply for mortgages in the next few months, remember to look over your credit reports to search for any inaccurate items that may be affecting your credit negatively. If you want some help with this process, reach out to CreditRepair.com.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263