Disclosure regarding our editorial content standards.

The National Council on Aging notes that reverse mortgages for seniors can be a valid part of an overall retirement plan. But they can also be complex financial tools, so it’s important to understand what you’re getting into if you choose to take one out. Find out more about reverse mortgages here to understand whether one might be right for you or your loved one.

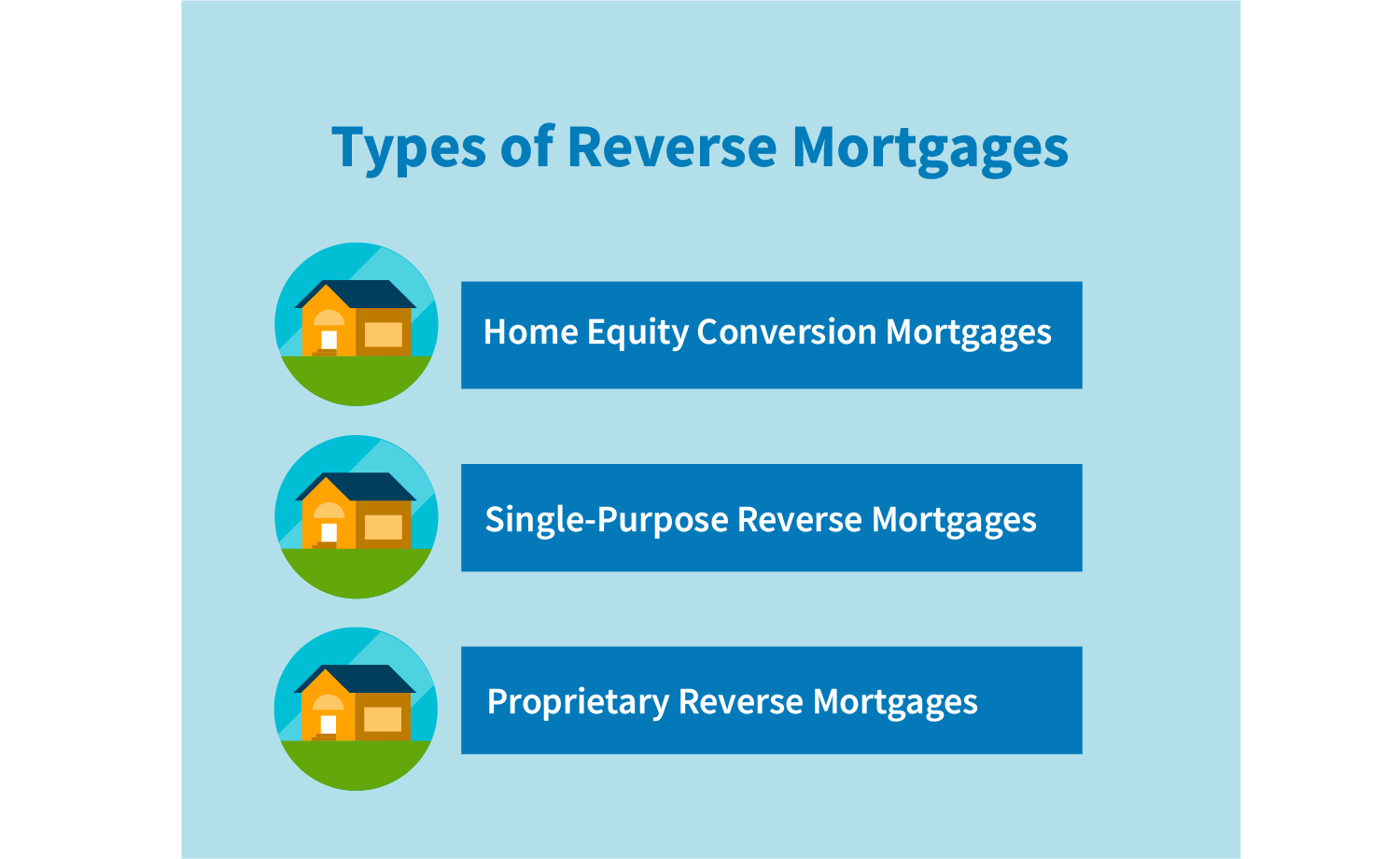

What Is a Reverse Mortgage?

A reverse mortgage is pretty much exactly what it sounds like. With a traditional mortgage, you borrow money to buy a home and make payments to the lender. With a reverse mortgage, you leverage the equity you have in your home and the lender pays you. Eventually, that money does need to be paid back, though, and details can depend on which type of reverse mortgage you opt for.

Home Equity Conversion Mortgages

Home equity conversion mortgages (HECMs) are backed by the federal government and available through FHA-approved lenders. To qualify for this program, you must:

- Own your home or have paid the mortgage down enough to have substantial equity

- Be at least 62 and live in the home in question as a primary residence

- Be able to demonstrate that you can pay charges associated with the home, including property taxes

- Be current on federal taxes and any other federal debt

The lender will also check your credit and verify other financial information, and you will need to participate in an information session with a HUD-approved HECM counselor.

How much you can get with an HECM depends on the value of the home, the current mortgage interest rate and the age of the youngest person borrowing. It is also limited by the HECM maximum amount of $765,600.

Single-Purpose Reverse Mortgages

The Federal Trade Commission calls single-purpose reverse mortgages “the least expensive option.” These types of reverse mortgages for seniors aren’t available everywhere and are offered through nonprofit organizations and some state and local government agencies.

Where available, these mortgages are typically reserved for those with low or moderate incomes. They’re also meant to be used for specific purposes as directed by the lender, such as paying off property taxes or providing necessary modifications or repairs to a home.

Proprietary Reverse Mortgages

Proprietary reverse mortgages are not backed by the federal government and are issued by banks or other lenders. In many cases, these are options for people with higher home values because the lenders can provide funds outside of the scope of HECM limitations.

How Do Reverse Mortgages Work?

The exact mechanisms of a reverse mortgage depend on the loan type and your agreement with a lender. But the typical basics are as described below.

- You take out a reverse mortgage based on how much equity you have in the home. If you own your home outright and it’s worth $100,000, you may be able to get a reverse mortgage for close to that much. If your home is worth $200,000 and you still owe $50,000 on it, that means your equity is $150,000. You may be able to take a reverse mortgage against part of that equity.

- You decide how you want to receive the money from the reverse mortgage. Options can include a lump sum, monthly payments as a form of ongoing income or a line of credit you can tap as you need.

- The money typically doesn’t have to be paid back as long as you are still living in the home as your primary residence. It will have to be paid back if you move out or pass away. The idea is that the home will be sold at that point and the proceeds of that sale can be used to pay off the debt.

Who Can Take Out a Reverse Mortgage?

In addition to things like the age requirement, there are qualifications for taking out a reverse mortgage that vary by type. Single-purpose reverse mortgages, for example, have income limitations. In all cases, similarly to qualifying for a traditional mortgage, you typically need a decent credit history and a certain amount of equity.

Is a Reverse Mortgage Right for You?

Only you can decide if a reverse mortgage is the right decision for you. Here are a few pros, cons and neutral points to consider when making a decision about this financial tool.

The Good

- A reverse mortgage can provide you with an immediate source of income or cash flow that can help pay bills, fund medical expenses or increase your enjoyment of retirement.

- You don’t have to sell your home—and move out of it—to get cash value out of it.

- The money you get isn’t taxable as income, even though you can use it as if it’s income.

The Bad

- A reverse mortgage is a one-shot deal that uses up the equity in your home. You won’t be able to tap into it again, and if you do sell your home in the future, you won’t likely get any cash out of the deal.

- Eventually, the money will have to be paid back. How much you owe back can increase over time due to interest.

- You do have to pay closing costs and other fees, just as you do with a traditional mortgage.

The In-Between

- Interest rates can change if you have a variable rate loan, and that can add a bit of chance to the equation.

Alternatives to Reverse Mortgages

Reverse mortgages are one potential way to fund your retirement. But before you apply for one, make sure you’ve considered all the options and that this is the right one for you. Some other options to consider are summarized below.

Pursuing Other Home Equity Financing Options

You may be able to get cash flow out of your home with other equity funding options, including a home equity loan or a HELOC (a home equity line of credit).

Refinancing Your Current Mortgage

If you have a mortgage still and the interest rate isn’t ideal, you might consider refinancing it. This could help you reduce your monthly mortgage payments, which would free up some money—plus, your home can still be an asset for you and your heirs.

Moving to a Less Expensive Home

Sometimes, moving out of a home makes the most sense. If the mortgage payment and upkeep is expensive, you could sell your home and move into a less expensive place. You would reduce your monthly expenses and could end up with extra cash from the sale of the home.

Final Tips

- Be aware of reverse mortgage scams. Stick to FHA-approved lenders or those with good reputations that you can trust.

- Take time to shop for the best terms to get the most out of your reverse mortgage.

- Talk to a mortgage counselor for help understanding your options and the terms of a potential reverse mortgage.

Consider checking your credit before you start shopping for a reverse mortgage, especially if it’s been a while since you last looked. Mistakes in reporting or even fraud might have caused inaccurate negative items to appear on your report, dragging down your score and reducing the chance you can get approved for a reverse mortgage. If you see anything questionable on your report, consider reaching out to CreditRepair.com to find out how we can help you put your credit history ship to rights again.