Disclosure regarding our editorial content standards.

Applying for a credit card can be an exciting event, but making sure you meet the requirements to get approved can make the process a bit more overwhelming. Fortunately, applying for a credit card is usually a quick process—especially in the age of the internet, when you can apply for a card from your couch.

Most requirements, like providing a Social Security number, are consistent across all cards. On the other hand, some cards may require a specific credit score or income threshold to be considered.

Here are the basics of credit card approval requirements.

| Credit card application requirements | |

|---|---|

| Age | 18 with a cosigner or 21 without a cosigner |

| Income | Verifiable income, either from a job or another source |

| Residency | Either a Social Security number (SSN) for citizens or Taxpayer Identification Number (TIN) for legal residents |

| Contact information | A physical address (usually no P.O. boxes), a phone number and an email address |

| Credit score | Technically no minimum, but scores lower than 600 could lead to rejections or higher interest rates |

| Other financial information | Employment status, monthly housing costs and bank account information |

Certain card issuers may have additional requirements, and you may be asked to show proof for some areas of your application—like a pay stub to prove your income, for instance. If you’re approved for a credit card, you’ll receive it shortly in the mail. On the other hand, if your application is rejected, you can call the issuer’s reconsideration line to appeal, explain your situation and make a case for approval.

Read on to learn more about how to successfully apply for a credit card and start building a strong credit history.

Basics of credit card approval requirements

Almost every credit card application will require several basic pieces of information, so being prepared with this information could make the process smoother.

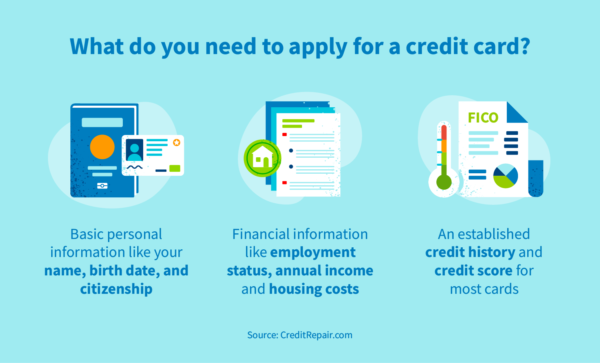

You’ll need to provide basic contact information, information about your finances and proof of residency and income to apply for a card.

Here are more specifics about what you’ll typically need to include on your application:

- Full name

- Birth date

- Current citizenship

- Social Security number or Taxpayer Identification Number

- Mailing address

- Email address

- Phone number

- Annual income (from any source, including nontaxable income)

- Employment status

- Monthly rent or mortgage costs

- Checking account information

If you’re looking to add an authorized user—someone who will also have access to the card—you’ll need to provide details about them as well. Finally, if you’re applying for a balance transfer card, which can help lower interest on credit card debt, you could be asked questions about the debt you want to transfer.

Once you’ve got all of your information together, you’re ready to apply for a credit card.

How to apply for a credit card

Most people apply for credit cards using online forms, but you can also request a paper form that you return by mail.

Before applying, though, you’ll need to figure out which specific credit card you want to apply for. Here are a few factors to keep in mind when choosing a card:

- Credit score minimums: You can typically find score ranges for successful applicants to various credit cards. Keep your own score in mind when determining which card may work best for you.

- Financial institutions: A variety of institutions offer credit cards. Some banks offer promotions to customers who use both banking and credit card services.

- Rewards and promotions: For those with higher scores, it is often possible to apply for credit cards that offer cash back or rewards points. Some credit cards may also come with initial incentives in the months or years after you open the card.

By determining what you’re looking for in a credit card and taking the time to look up your own credit score, you’ll be able to look around for the best fit for you. Some of the card specifics—like credit limit and interest rate—will depend on your application, as the card issuer will generally determine your risk to set these numbers.

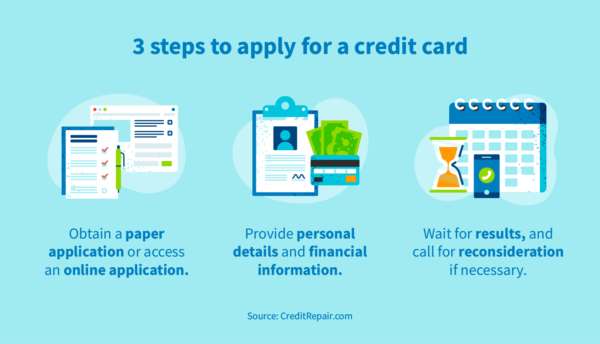

When you’ve picked a card, it just takes three simple steps to apply:

- Get a paper application or visit the online application form for the card you chose.

- Fill out the application with your personal information, contact information and financial details.

- Wait for results, which are often immediately available online. If you’re approved, wait for your card in the mail, and if you’re denied, you can call the reconsideration line or apply for a different card.

Be careful about applying for too many credit cards in a short period of time, as these “hard inquiries” to your credit report could cause your score to fluctuate.

What to do after applying for a credit card

After you apply for a credit card, you should hear back fairly quickly whether you’ve been approved or not. With online applications, you may even get instant approval with the right financial history.

Here’s what to do next:

- If you’ve been approved, you can start using your card soon. Make sure you use your card in a way that will help your score grow: make on-time payments and try not to spend up to your limit.

- If you’ve been denied, you can call the card’s reconsideration line to ask for another chance. If you’re still struggling, you may want to apply for other credit cards or look at the factors that may have led to the denial.

You can be denied a credit card for any number of reasons, though there are a few common reasons. For example, you may have a high debt-to-income ratio—in other words, the card issuer could be worried that your current income may not be enough to take on more debt. Alternatively, you may have a spotty credit history, because of either missed payments or a lack of credit usage.

If you haven’t had much access to credit in the past, it can be hard to get approved for a credit card. Consider using a secured credit card, which helps you build credit but generally has fewer approval requirements.

For those with poor credit history, one of the best options can be working with a credit repair company. The professionals at these companies can help review your credit report and work towards a plan to rebuild your credit. Additionally, if any inaccurate information is found on your credit report, a credit repair company can help you file a dispute to petition to have it removed.

In any case, getting approved for a credit card can be an important financial milestone, so keep working until you’re able to reach your goal.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263