Having a joint credit card account can be a good idea for many different reasons. When two people share an income or expenses, only having one account to balance at the end of the month can simplify things greatly. Joint credit also offers a number of lesser-known benefits, like helping a partner improve their credit or get approved for a card they wouldn’t be able to get on their own.

Of course, joint credit also comes with risks: both people on the account are equally liable for any late payments or other mistakes, and giving equal access to each person’s finances can cause problems in the relationship if spending habits are different.

We wanted to know how many people are willing to take on a joint credit card, and at what point in the relationship they would be willing to do so. We also asked what people’s primary reasons were for opening a joint account.

Here were some key takeaways:

- 1 in 3 people would not share a credit card with a partner

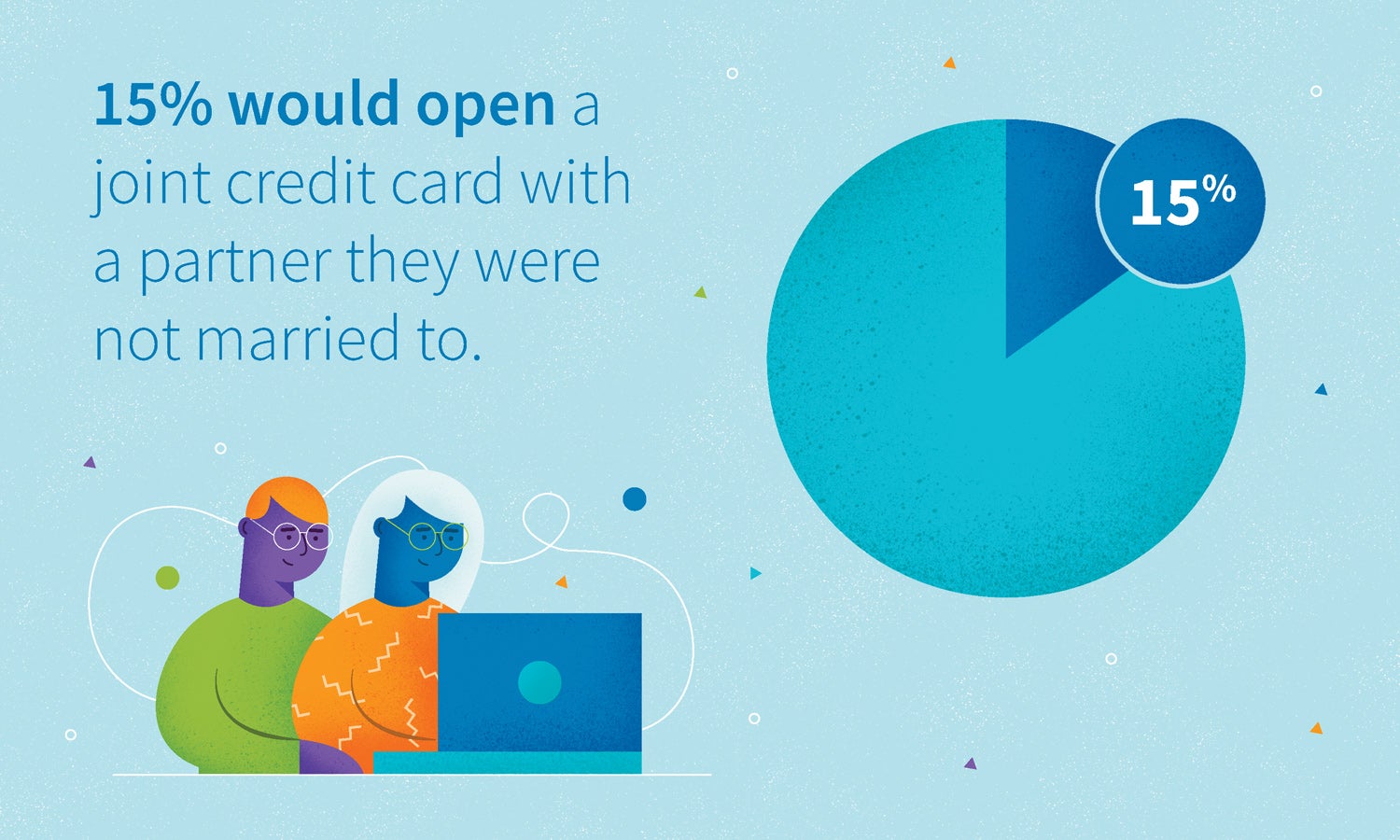

- 15% would open joint credit with a partner they were not married to

- Fewer than 1 in 5 would use a joint account as a tool to improve credit

Many People are Independent Borrowers

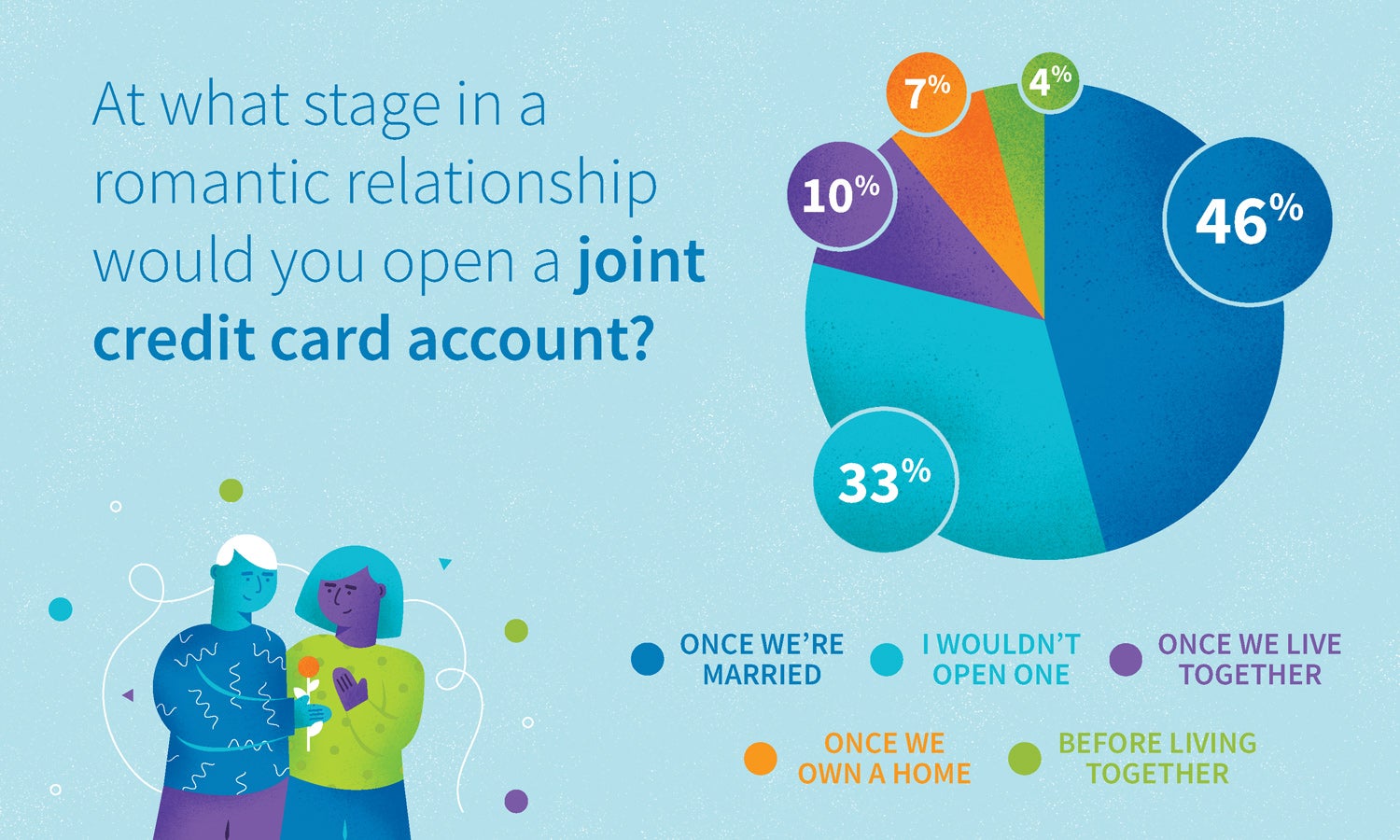

A surprising 33 percent of respondents said they would not open a joint credit card with a partner at all, despite the many potential benefits of sharing an account.

It’s possible that the stigma associated with shared finances — that it’s a recipe for relationship trouble and, eventually, will complicate the divorce — prevents people from thoroughly researching the actual risks that come with sharing credit. But in fact, one study published earlier this year in the Journal of Consumer Psychology showed partners’ spending habits actually improve when they share accounts. A similar study by Lexington Law also found that 29 percent of people believe their partner influences them to spend less, rather than more.

This high number of independent borrowers may also be due to some banks’ recent decision to stop issuing joint credit cards. CapitalOne, HSBC and JPMorgan Chase no longer allow joint credit cards, which could be why so many borrowers opt to keep their accounts separate.

Waiting Until Marriage…to Share Credit

Though joint credit accounts can be powerful tools for improving financial health, entering into a shared financial commitment at the wrong time or with the wrong person can have major consequences.

In our survey, 15 percent said they would be willing to open a joint account with someone they were not married to. Of those respondents, 11 percent said they would open a joint account once they lived with their partner, while 4 percent said they would share credit even before sharing a home.

A major component of responsibly sharing credit is making sure both partners share the same financial attitudes, which includes similar spending and saving habits, compatible financial goals and healthy communication patterns.

Each person on a joint account is individually liable for that credit, which means that if a partner leaves the account, the other person will be held solely responsible for paying the balance on it — whether or not they were the person who spent the money. In the worst-case scenario, this can result in seizure of a person’s savings, car and even home in order to cover their partner’s spending.

Opening a joint account in the early stages of a relationship may feel like a good idea at the time, but can become disastrous down the line. Waiting until the relationship is mature and being sure to talk explicitly about both partners’ financial expectations for each other can help ensure a couple’s financial success.

People Aren’t Aware of Joint Credit’s Benefits

Many assume the only reason to open joint credit is to simplify finances within a shared household, and while that is one of the bigger benefits of consolidating credit, opening a joint credit card can also be a strategic move to improve credit scores.

Joint credit can also offer benefits to both partners’ individual financial health, provided that their spending habits are similar and they are willing to get on the same page about shared financial goals. In single-income households, it can be difficult for the non-earning partner to get approved for a credit card on their own. Opening a joint account is one way to get approved for credit without a salary.

If past credit mistakes have resulted in someone having a much lower credit score than their partner, opening a joint credit card can be a good way for them to improve their credit. Since joint credit appears on both people’s credit reports, good borrowing habits will be reported on both people’s credit histories.

However, if someone has serious past credit mistakes, their partner should be very cautious about making absolutely sure they’ve developed better spending habits before committing to sharing a credit account. The best way to make sure you repair credit responsibly and avoid any backsliding is to work with a specialist who can recommend the best strategy to improve financial health for both you and your partner.