During the spring of 2019, CNBC reported that the average American family had around $8,800 in accounts with credit unions or banks. But even those with higher numbers didn’t meet what experts consider a safe zone.

The reality is that many people don’t have this type of financial buffer. In fact, around 40% of Americans didn’t have $400 saved for emergency expenses in May 2019, according to the Federal Reserve. And we get it—keeping money in savings can be hard! If you find yourself in an emergency and have to rely on your credit cards, here are some things you should consider.

How to Use Your Credit Cards During an Emergency

If you’re considering using credit cards to help stabilize your cash flow and cover immediate expenses, make sure you’re watching your credit utilization rate, capable of paying your minimum monthly payments, and using cards with the lowest interest rates and fees. Some other best practices include:

- Using the right card to maximize your benefits and minimize your costs.

- Repairing your credit before applying for or using an emergency card.

- Asking for a credit limit increase on an existing card before you apply for new cards.

The better your credit is, the more likely you’ll be able to get a card with a lower rate or better perks. But there are also credit cards for poor or bad credit that might offer a much-needed lifeline in situations such as natural disasters or the coronavirus pandemic.

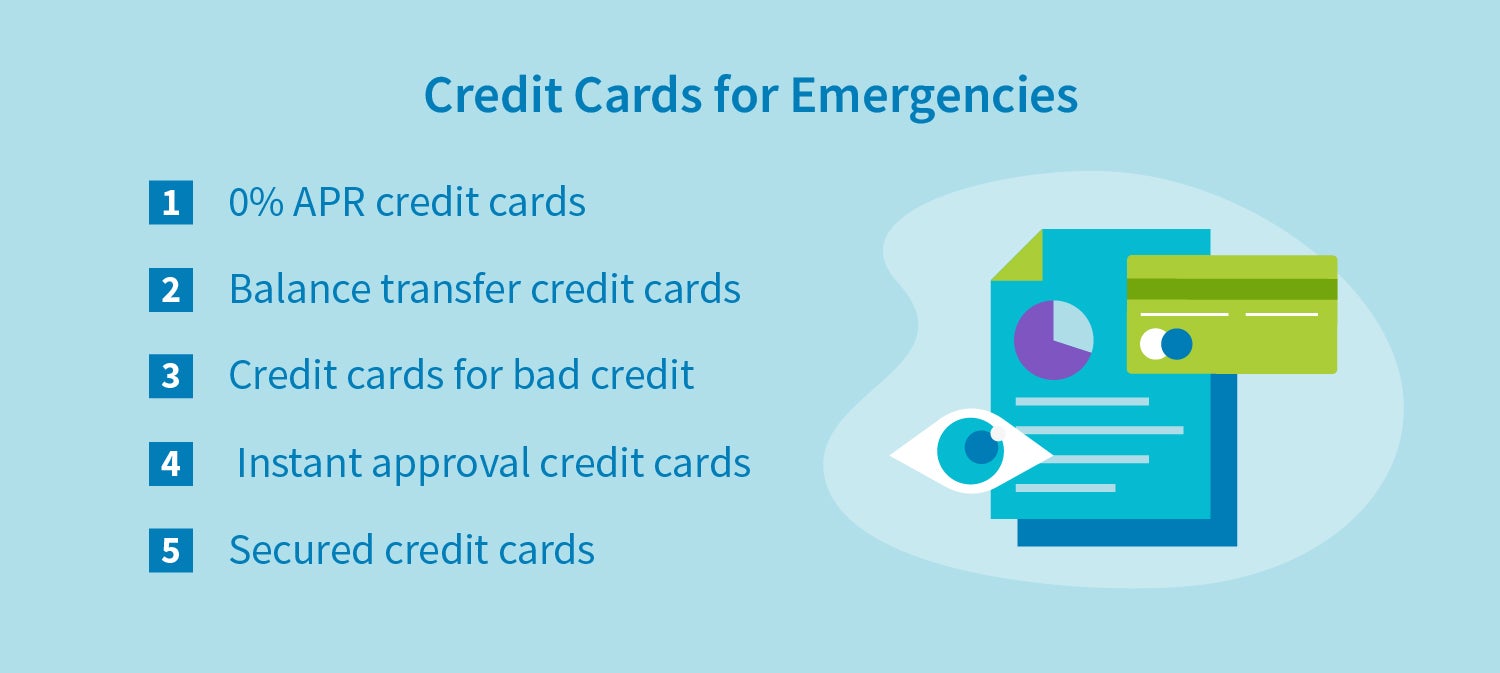

0% APR Credit Cards

For those with good enough credit, 0% APR credit cards might be a good tool to use during this time. These cards come with a low introductory APR of 0%. That means you pay 0% in interest on purchases for the introductory period, which typically ranges from six to 21 months and depends on the card.

Pros: These cards let you spread emergency expenses for one or two months over the entire introductory period without additional cost. For example, if you need to cover $4,000 in expenses during two months of an emergency, you can use a 0% APR card with a 15-month introductory period. Then, you can pay around $267 a month on the debt, which might be more doable if you have a lower income.

Cons: That being said, you typically need good or excellent credit (670 – 800+) to get approved for these offers. No credit offer is ever a sure thing, though. Even people with good credit get denied sometimes.

Balance Transfer Credit Cards

Sometimes, it’s your credit card bills you need help covering during an emergency. Balance transfer cards might be the answer for this situation.

Pros: Balance transfer cards offer a lower APR—often 0%—for a period of time on balances you transfer from another card. This can save you a lot of money and offer some flexibility in how you manage your debt.

Cons: Moving the balance from one card to another means you now have two cards. And the old one no longer has a balance—or it has a smaller balance, which leaves some credit available, which could potentially lead to double the debt.

Credit Cards for Bad Credit

If you have a low credit score, you might not qualify for low introductory offers or balance transfers. You might also be limited to cards with lower credit limits.

Pros. These cards are often approved even if you have bad credit or negative items on your credit report. They might also offer a chance to build credit, as the lenders typically report timely payments to the credit bureaus.

Cons. Credit cards for bad credit may not offer much assistance for covering emergency expenses if your credit limit is very low. If you have time, it might be better to attempt to repair your credit enough so you might qualify for a better option.

Instant Approval Credit Cards

Instant approval credit cards are those that you can apply for and receive a decision in real-time. Typically, you apply online and receive an answer within seconds about whether or not you qualify for the card. These types of cards are generally reserved for those with credit in the “good” range.

Pros. In an emergency, you need answers quickly. You might not be able to wait a few days to know if this is a tool you can use, so immediate answers are helpful.

Cons. Each time you apply, the lender conducts a hard inquiry on your credit report. Each hard inquiry can knock your credit score down a bit. That means multiple applications can make it harder for you to get approved for credit in the future, so be careful about how many times you apply—even in an emergency.

Secured Credit Cards

Secured credit cards are designed for those with bad or no credit. They have lower credit requirements, but you do have to put up a deposit before you’re approved for the card.

Pros. You might be able to get approved for secured cards even if you can’t get approved for any others. They can also help you build a more positive credit history, especially if you choose a lender that reports to all three bureaus.

Cons. You have to put up money to get one of these cards. That means they might not be the most ideal tool to help you cover emergency expenses in the short term.

Credit Card Offers to Avoid

You might be facing an emergency financial situation, but that doesn’t mean you should ignore the fine print. Avoid credit card offers with high interest rates or annual fees. Those accounts could end up increasing your overall expenses, which won’t help with emergency debt management or cash flow.

It’s also a good idea to make sure you understand the benefits that come with the cards. Carefully check what benefits you would be getting with any credit card you’re considering.

In addition, check whether credit card insurance is available as an option so you can make the most educated choice. You’ll want to compare different policies and decide which, if any, fit your situation. As you navigate the obstacle course that is choosing a credit card (or credit cards), it’s a good idea for you to keep an eye on your credit score before, during and after the process. Fortunately, if you’re looking for assistance, there are credit consultants who can help you with this.