DIY credit repair consists of a series of steps that you can take on your own to improve your credit score and reap the benefits of a higher score. Poor credit history can make for a difficult future so it’s essential that you take credit repair seriously if your credit score is less than ideal. Poor credit can deny you access to loans, credit cards and other forms of credit. Sometimes potential employers will also take a peek at your credit history before hiring.

It may sound like a lot to take on, but you really can actively improve your credit. To prepare for your credit repair process, make sure you have these documents and info handy:

- Your Social Security number (SSN)

- Your name and DOB

- Your address

- Account information

- Online access to your accounts

Below we’ll cover important steps to repair your own credit.

1. Obtain your three free credit reports and credit score

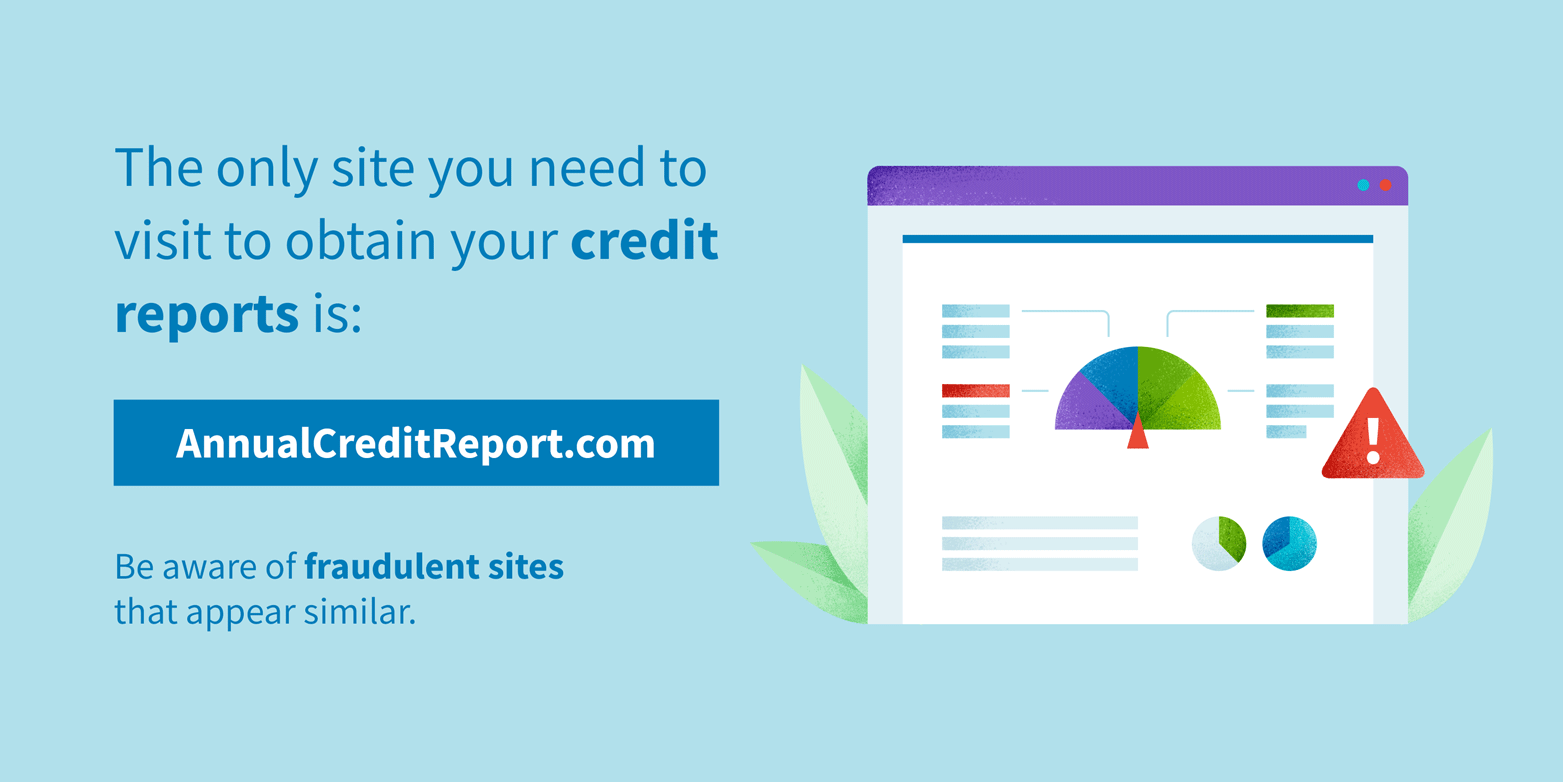

There are three major credit bureaus that review consumers’ credit history: Experian, Equifax and TransUnion. Under the Fair Credit Reporting Act (FCRA), each of these bureaus is required by law to provide you with one free credit report each year (due to COVID-19, you can now access a free copy of your credit report each week until April 2021.)

These reports itemize your credit history so you can see what items are bringing your credit score down. You can spread these free reports out throughout the year, but if you’re repairing your credit you’ll want to access them all to get a better understanding of where you stand with each bureau. It also doesn’t hurt to access your free credit score from a verified site or your credit card lender if they offer that service.

You should be very wary of fraudulent sites. The only site you’ll need to visit for your free credit reports is AnnualCreditReport.com. Fraudulent sites try to trick consumers into sharing valuable personal information, so stick to the resources approved by the Federal Trade Commission (FTC).

2. Examine your credit reports

Review each of your reports carefully and look for items that can damage your credit, like:

- Typos or errors in your personal information

- Late payments

- Maxed out accounts

- Unknown accounts (could be a sign of fraud or ID theft)

- Accounts you requested to close, but are still open

- Accounts that have gone to collections

Make sure to document each negative mark you find and which account or creditor it’s attached to. You’re going to need to address each negative mark against you.

3. Address accurate negative marks

If there are accurate negative marks on your credit report, you’ll need to address them with your creditor—not the credit bureaus.

There are two ways to remove accurate negative marks from your credit report: time—you let the marks fall off of your credit report—or by reaching out to your creditors. Your creditor is not obligated to remove an accurate negative mark, but in some instances they may.

For example, you can ask your creditor to help you resolve delinquent payments and accounts by setting up payment plans or creating another solution with your creditor. Taking care of past-due payments and unwanted accounts can have a positive impact on your credit.

Or, if you are ordinarily in great standing with your creditor and have a consistent history of making payments on time but — due to an unusual situation – made a late payment that is now on your credit history, you may be able to reach out to your creditor using a goodwill letter and ask that they remove it as a courtesy.

4. Dispute false items to have them removed

If you find inaccurate, negative items on your credit report, you can reach out to the credit bureau who reported them and dispute them.

There are a variety of ways to file your credit dispute including online, over the phone and by mail—the preferred method depends on the bureau. Any items that you’ve determined to be false (including incorrect personal information) should be included in your dispute to the bureau who falsely reported them. Here are some examples of inaccurate, negative items and what you can do to dispute them.

Unclosed accounts

If you see that an account you requested to close is still open, you should contact the lender and ensure that the account is in fact closed. If it is, that would be a false item that you can dispute.

Unknown accounts

If there are accounts open in your name that you don’t know about, that could be a sign of identity theft or fraud. You should immediately contact the organization that account is held under, start an investigation and work with them to have the account removed. As a best practice, keep records of your communications as they may be useful in an identity theft investigation.

If your claim is accepted, the bureau should remove the negative item which, depending on your credit profile, could help boost your credit score. If the bureau doesn’t remove the item, you’ll need to work with the bureau to request that the inaccurate reporting be removed.

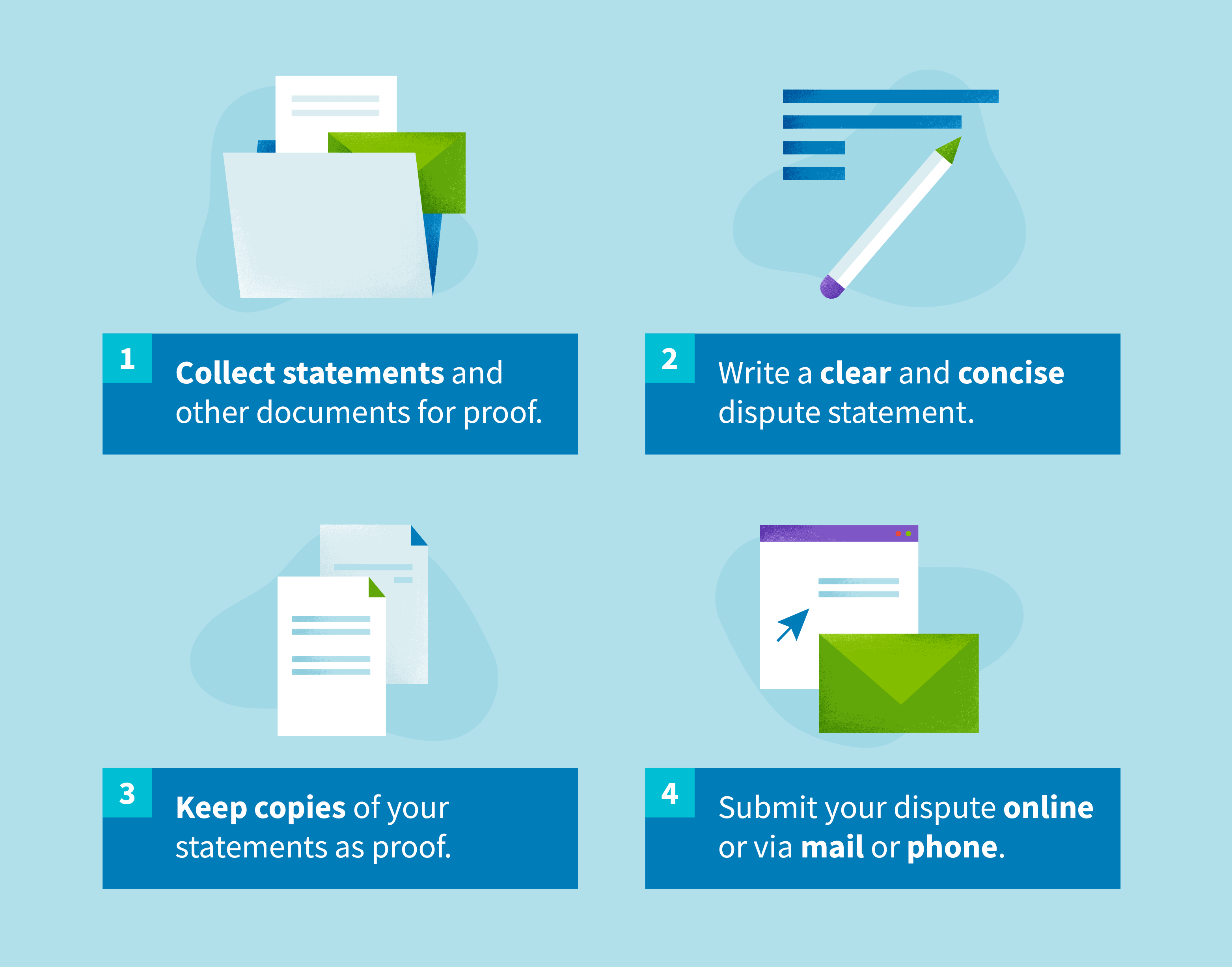

Here are the steps you should take for a successful resolution:

- Collect proof (statements and other documents) to support your dispute.

- Write your dispute statement. Make your dispute letter easy to follow by first listing the items you’re disputing, then going through them one-by-one and explaining the reasoning and officially requesting their removal. Include copies or snippets of supporting documents where necessary.

- Document your dispute with copies of your statement. Save screenshots if you complete your dispute online and make sure to get verified mail if you decide to mail your statement.

- Submit your dispute and stay tuned for the results of their investigation. The easiest way to document and track the progress of your dispute is by submitting online. Use the table below to find the contact information you need to submit your dispute by your preferred method.

5. Review their decision, respond if necessary

Bureaus have 30-45 days to respond to you from the day they receive your dispute statement. During this time the bureau sends your statement and relevant information to the organization who reported the initial claim, then that organization investigates the dispute and sends its findings to the bureau. Once the investigation is completed, the bureau will send you the results.

Once you receive the result of your claim, you should review it thoroughly. If the results are in your favor, congrats! The bureau will handle removing the negative item from your report.

What do you do if your claim is denied?

If the results are not what you expected, you can take additional steps, including:

- Contacting the lender directly who reported to the bureau and gain additional information (if needed).

- File a new dispute with the bureau that includes new information so the bureau can approach the creditor with additional evidence.

- Add a consumer statement to your credit report. You can request that the bureau adds a statement (100 words or less) to your credit report that explains your situation. This means any entity that accesses your report will also see your consumer statement along with it. Just remember to contact the bureau to have it removed if and when the negative item is removed from your report.

- Bring your issue to a higher authority. If you’ve hit a wall and believe that there will be no fair resolution, you can submit a complaint to the Consumer Financial Protection Bureau or even consult an attorney, depending on the situation.

6. Avoid applying for many new lines of credit at once

While your credit is being repaired, you’ll want to avoid requesting new lines of credit if possible. Every time you apply for credit it’s seen by the credit reporting agencies as a “hard inquiry” which factors into your report and score. If you apply for a new line of credit many times in a short span of time (for example, if you apply for a new credit card repeatedly because you’re having a hard time being approved) it can negatively affect your credit score.

People with good credit scores can apply for credit a couple of times a year without having it affect their credit greatly. While you’re rebuilding your credit, be careful about any hard inquiries.

7. Stick to good credit habits

Continually practicing good credit habits will eventually return a positive result, regardless of how your claim turned out. Try to turn these practices into habits to improve less-than-ideal credit and maintain good credit.

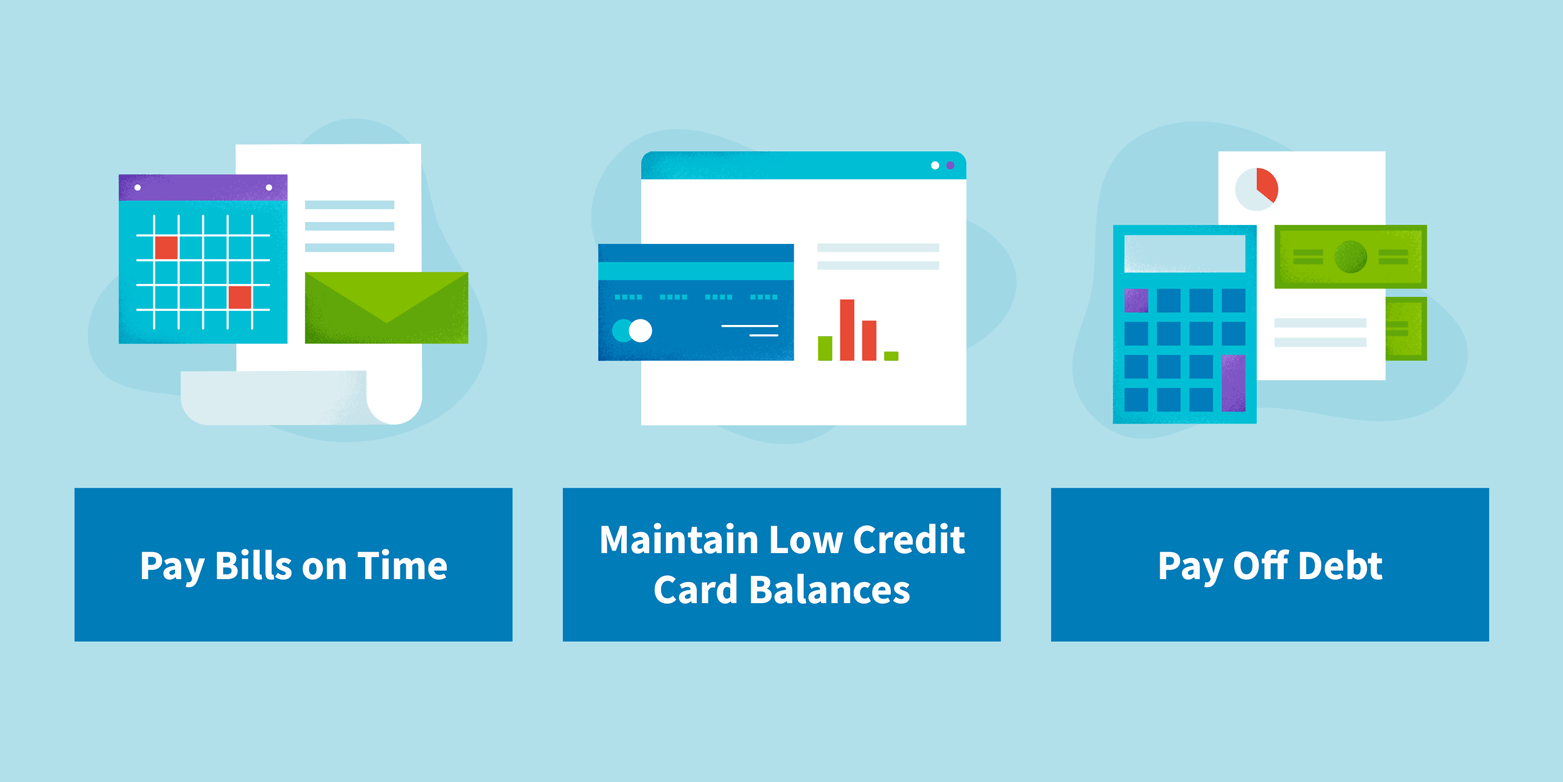

Pay bills on time

Pay your bills on time to protect your credit from additional dings. Payments that are 30 days late are subject to be reported to the credit bureaus. Minimum payments will protect you from late fees, but not from interest. You should strongly consider enrolling in bill auto payments if you aren’t already.

Pay off debt

Paying off debt is a huge step in the right direction. There are different approaches you can take in order to pay off your debt:

- Adjust your spending habits. If you haven’t gone into default yet, adjust your budget and spending patterns to, at the least, make minimum payments. The more you can pay off of credit card debt and loans, the better.

- Consider consolidating your debt. Debt consolidation involves taking out one loan to pay off all your debt and then paying off that loan in place of multiple payments with higher interest rates.

- Talk to your lender. If you’re having trouble keeping up with your payments, your lender may be willing to negotiate a new agreement and payment plan that’s more manageable.

Maintain low credit card balances

Keeping your credit card balances low can have a direct and positive impact on your credit score. The amount of credit debt you have compared to your credit limits is called your credit utilization, which accounts for 30% of your FICO score and 20% of your VantageScore. This also means that you shouldn’t borrow more credit than you can afford to pay off.

Stay patient and consistent while rebuilding your credit. Stick to the responsible credit habits listed above to see your credit score improve. Once you’ve paid off your debts and have a good handle on proper credit habits, you can start building new credit to help boost your score with positive tradelines and positive habits.

DIY credit repair resources

Below are helpful resources to help you pay off debt and repair your credit.

- Federal Trade Commission (FTC): Credit Repair Guide (PDF)

- Federal Reserve: Credit Score Tips (PDF)

- FTC: Avoiding Credit Repair Scams

- FTC: Settling Credit Card Debt

- IdentityTheft.gov: Identity Theft Letter to a Credit Bureau

- USA.gov: Debt Resources

Credit repair can be a complicated process depending on your individual circumstances. If you’re worried about being able to properly address your credit repair, you may want to consider looking for assistance. Try a free credit report consultation to see where you stand and let our experienced team take over the heavy lifting.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263