Disclosure regarding our editorial content standards.

This guide will take you through how to file self-employment taxes step-by-step, with some essential tips and tricks you can keep in mind for future years.

Understand the basics of self-employed taxes

You’ve probably heard that all income is taxable. That’s essentially true, but there’s a minimum amount you have to earn to qualify for paying taxes. Individuals have to file a tax return if they earn self-employment income of at least $400.

To calculate your self-employment income, you’ll need to gather all your invoices from the tax year and add up the totals. Freelancers are encouraged to keep a running spreadsheet of their invoices throughout the year to make sure they don’t miss anything or make mistakes. The total amount for the year is your total annual income.

If you charge a client $600 or more in a year, they’ll owe you a 1099-NEC Form. (Note that before 2020, the 1099-NEC Form was called the 1099-MISC Form.) This Form will summarize the total services you charged them for a tax year. You should check these 1099-NEC Forms against your records and make sure they match up.

Clients who pay via electronic service providers such as PayPal may choose to send you a 1099-K Form instead of a 1099-NEC. Both of these Forms are similar and should be used to help calculate your total income earned.

However, don’t count on receiving every 1099-NEC or 1099-K Form you’re due. It’s quite common for clients to forget to send these out, so you must have your own records to rely on. Not receiving these Forms is no reason not to include that income on your tax return.

Lastly, an essential part of filing your taxes is understanding your tax classification. You’re self-employed if you’re an independent contractor or in business for yourself. However, if you’re a business owner who hires or contracts individuals to provide services to your business, your tax classification is a business owner.

The tax breakdown

Self-employed individuals must file an annual tax return and—sometimes—pay estimated quarterly taxes instead of paying taxes just once a year.

Taxes for self-employed individuals are broken down into two main categories: self-employment tax (SE tax) and income tax. When a person works for an employer, Social Security and Medicare taxes are withheld from their wages by their employer. However, when a person is self-employed, the SE tax is their way of contributing to Medicare and Social Security taxes.

The self-employment tax for 2021 is 15.3 percent of net earnings. This number is a combination of 2.9 percent paid for Medicare and 12.4 percent for Social Security tax. In 2021, everything up to $142,800 is subject to the 15.3 percent total SE tax. Anyone earning above $142,800 only has to pay the 2.9 percent Medicare tax. However, single filers earning above $200,000 (or joint filers earning above $250,000) may have to pay an additional 0.9 percent Medicare tax.

In addition to SE tax, there are also standard income taxes due for the self-employed.

The tax Forms you’ll need to use

Individuals who work for an employer typically get a W-2 Form for their taxes showing everything they earned. However, this isn’t the case for the self-employed. Instead, the main tax Form you’ll use to file your self-employed taxes is Form 1040, which you fill out yourself.

The Form 1040-ES, Estimated Tax for Individuals helps self-employed people determine how much they owe every quarter (paying quarterly is a recommended way of approaching taxes instead of paying once, yearly). This Form also has vouchers you can use to process the amount owing to the IRS.

You’ll also want to file a Schedule C Form to report your business profits and a Schedule SE to calculate your self-employment taxes. Your clients may send you 1099-NEC Forms or 1099-K Forms, which you’ll want to compare to your own records.

The deadlines—paying taxes quarterly

Individuals working for an employer only have to pay their taxes annually because the employer withholds income and other taxes from their paychecks. However, self-employed individuals receive all their gross income up front and must make more frequent payments to the IRS. The IRS wants its money throughout the year, so self-employed individuals usually make estimated quarterly payments.

You only have to pay quarterly taxes if you estimate you owe more than $1,000 in taxes per quarter. The deadlines for quarterly taxes are:

If the deadline falls on a weekend or a holiday, taxes are due on the next business day.

Individuals can always choose to pay their taxes early and not wait for the deadline to file.

Avoiding the quarterly deadlines and only paying your taxes annually can potentially result in you being charged with an estimated tax penalty.

How to file

You have a few options when it comes to filing your taxes. You can opt to do them yourself (usually using a program like TurboTax or TaxAct), or you can hire a tax professional to file on your behalf. If your taxes are complicated, hiring a professional is usually a worthwhile investment. But if you think your taxes may be relatively straightforward, filing yourself can save you some money.

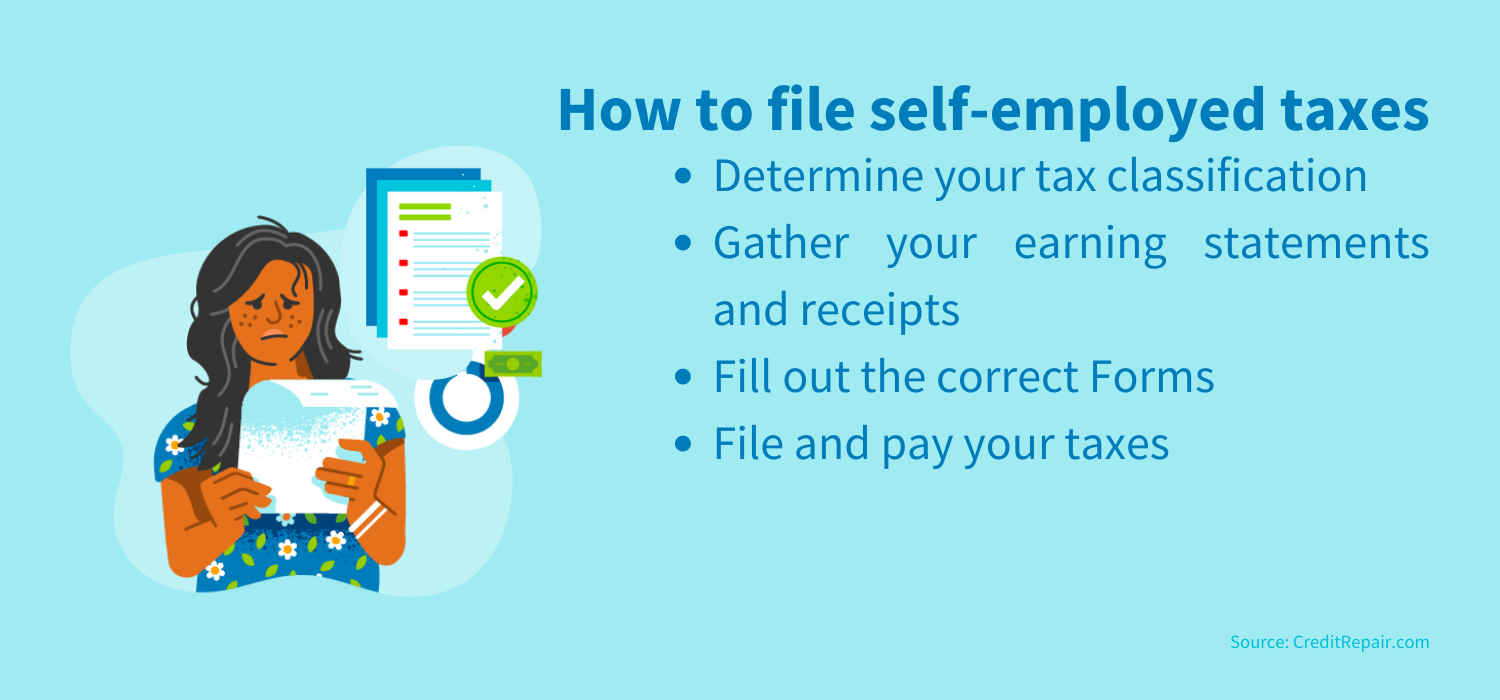

4 steps to file

The four steps to filing self-employed taxes are:

- Determine your tax classification: First, you want to confirm that you should be filing as a self-employed individual. The IRS defines a self-employed individual as:

- Someone who carries on a trade or business as a sole proprietor or an independent contractor

- Someone who’s a member of a partnership that carries on a trade or business

- Someone in business for themselves (including a part-time business)

- Gather your earning statements and receipts: The next step is to calculate your revenue and expenses for the year. You can collect your 1099-NEC and 1099-K Forms and compare them to your records to determine your total income. As a self-employed individual, you can claim a lot of tax deductions for your business. You’ll want to gather all your receipts for expenses paid throughout the year so you can claim them and make sure you have the proof. You can claim business-related travel, entertainment, gifts and transportation expenses.

- Fill out the correct Forms: As we mentioned above, you’ll need to fill out Form 1040, Schedule C and a Schedule SE Form for your self-employed taxes.

- File and pay your taxes: Once your Forms are filled out, you’ll want to file them with the IRS. Note that if you believe you owe at least $1,000 in taxes per quarter, you’ll be filing and paying your taxes each quarter. You can pay your quarterly taxes one of the following ways:

- Via the vouchers on the 1040-SE Form

- Through an Electronic Federal Tax Payment System with your bank account information

- By debit card or credit card through an IRS-approved service provider

Is there an optional filing method?

Some self-employed individuals qualify for an optional filing method that gives them credit towards their Social Security coverage, increases their earned income credit or increases their child and dependent care credit.

The optional filing method only applies to self-employed individuals who lost or earned a small amount of income. The Schedule SE Form clarifies who’s eligible for optional filing.

How to prepare to pay self-employed taxes

It’s essential to have a plan to pay your taxes so you aren’t surprised with a hefty bill every quarter. Self-employed individuals should follow these steps to prepare for payment:

Set aside around 30 percent of your income

The general rule of thumb for self-employed people is to reserve 30 percent of their income for taxes. Remember that you’re paying for a combination of income tax and self-employment tax, which is why the percentage is so high.

Some individuals will need to save more or less depending on their personal circumstances. If you’re working with a pro, they can help you with this estimation. Additionally, after a few years, you’ll better understand how much to put aside based on your average earnings.

It’s imperative to put this money aside as soon as you get paid so you don’t spend it and end up in a situation where you can’t pay your taxes. Freelance income can be very sporadic, so watch out for the trap of thinking you can spend now and earn what’s owed on your taxes later on.

Most people recommend a budgeting system of automatically moving the 30 percent into a separate account reserved for your taxes.

Keep track of all your expenses and sources of income daily

Since you don’t have an employer that will sum up everything for you, you need to track all your income sources and expenses. For example, you might work with dozens of clients in a year. Remember to keep careful track each client, how much you charged them and when they paid so you can report your taxes accurately.

Identify what deductions you can take

Self-employed individuals are eligible for a wide range of tax deductions that a regular employee can’t claim. Some of the most common ones include:

- Office supplies

- Travel expenses (hotels, plane tickets, mileage, etc.)

- Home office expenses

- Business-related meals

- Advertising and marketing

- Computer equipment and software

- Utilities (internet, phone)

- Health insurance

- Legal services

- Contract services

- Licenses

You’ll have to look into each individual deduction to understand better if you qualify.

Pay as much as you can

Ideally, you’ll pay everything you owe. But if you can’t pay everything at once, it’s still important to file. You’ll have to pay what you can and then discuss your situation with the IRS. You may receive an extension, get some of the penalties waived or be able to sign up for an IRS Online Payment Plan. The IRS will work with you to address your tax debt, so don’t ignore it.

The consequences of not paying taxes are serious. You can receive late fees, incur interest and even get to a point where your wages are garnished.

Consider working with a tax professional

Self-employed taxes are complicated, so it might be a good idea to work with an accountant. Even if you think you have a handle on the tax process, the IRS changes it quite frequently (such as the switch to the 1099-NEC Form we mentioned earlier). For these reasons, hiring a tax professional is often the best route for self-employed individuals.

Protect your finances

It’s crucial that you take care of your finances in all regards. Along with keeping up with your taxes, you want to make sure you maintain a good credit score, pay off debt and save for retirement. A strong financial standing will help you in many areas of your life, such as securing mortgages, auto loans, personal loans and credit cards and passing credit checks from employers.

Learn more about steps you can take to care for your financial health at CreditRepair.com.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263