Disclosure regarding our editorial content standards.

You’re likely already aware of the detriments attached to having a low credit score. Poor credit can make many of life’s major milestones far more difficult—whether buying a home, financing a car or simply opening up a credit card, lenders are far more hesitant to consider you as a reliable candidate if you have a bad credit history. Even if you do get approved, get ready for sky-high premiums and interest rates that make for a tougher financial burden.

What you may not realize is that having a poor credit score can impact more than just your wallet. When faced with mounting financial setbacks, the consequences of a bad credit score can start to hinder you mentally and physically. Your mental health, personal relationships, and overall lifestyle can all suffer as a result of a poor credit score.

If you think your mental and physical well being are being negatively impacted by your financial situation, our infographic outlines some healthy habits and acts of self-care you can implement into your routine to help combat the unwanted side effects of financial stress.

1. Stress

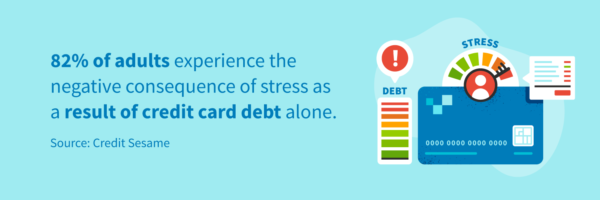

Close to two-thirds of adults reported in 2020 that money is a significant source of stress in their lives. Considering that your credit score impacts your level of access to various major lifestyle opportunities, this doesn’t come as a surprise. Additionally, a 2020 report by Credit Sesame found that 82 percent of adults experience the negative consequence of stress as a result of credit card debt alone.

There are a number of reasons for financial-induced stress, especially when it comes to high amounts of credit card debt. For many, it means losing eligibility to obtain a credit card, which they may have been leaning on to fund their lives. For others, their credit card debt impacts their ability to qualify for a home mortgage or a car loan. It could also mean the inability to fund a child’s college education, contribute to retirement savings or pay off student loans.

2. Fatigue

Poor credit health is also linked to fatigue and sleep loss among many adults. A 2020 study by Bankrate found that 48 percent of Americans lose sleep at night due to a financial constraint. 13 percent of those reported their ability to pay their credit card debt as the sole cause of their sleep loss. Additionally, 20 percent of Americans said they felt physically ill at least once a month in 2019 due to the debt they carry.

Individuals who are struggling to pay their bills, afford their cars and homes, or sufficiently fund their children’s education may also be working considerably longer hours in order to make ends meet, which ultimately results in less time available for sleep and rest. Even if they aren’t working overtime, constantly worrying about their finances can keep them up at night even when they’re physically tired, keeping them from getting the quality sleep they need.

3. Anxiety

Having a high credit score enables you to secure loans at lower interest rates or borrow large sums of money in a pinch. This includes being able to pay for unexpected health emergencies, which may include an ambulance ride, seeing medical specialists or undergoing surgery—events that can quickly rack up to thousands of dollars. But if you have poor credit, it’s less likely that you’ll be able to fund such major expenses.

A 2020 study found that Americans indicated the rising cost of healthcare as their top financial worry, and 79 percent of them cited feeling anxious about it. Additionally, Credit Sesame’s 2020 report stated that 58 percent of adults said they would use a rideshare service to get to the hospital to avoid the high costs of an ambulance.

It’s hard to argue the fact that maintaining your health—and being able to afford the costs associated with it—is a crucial part of having peace of mind in all aspects of life. It’s no surprise that mounting anxiety is a serious side effect of high healthcare costs and whether or not you have a high enough credit score to cover them.

4. Shame and guilt

A less-often discussed side effect of poor credit health or debt is the feelings of shame and guilt they can induce—a 2020 study of individuals with poor credit showed that 46 percent of them felt ashamed about it. A 2019 study of individuals in debt revealed that 49 percent of respondents blamed themselves for credit card debt, and 33 percent did so for a personal loan. This often leads to ruminating thoughts—”How could I let things get this bad? Why did I allow myself to end up in this situation?”—that only exacerbate the pervasive feelings of guilt that come with a lack of financial stability.

Additionally, appearances of wealth and materialism are inextricably linked to how society and culture perceive others’ level of success. It’s not uncommon for those with large amounts of debt to feel embarrassed about it, believing that they don’t measure up compared to their debt-free peers. This can lead to a vicious cycle of racking up more debt and further driving their credit score down in an effort to portray a false image of success through expensive clothes, flashy cars and costly nights out—all to keep up with appearances. Unfortunately, this only heightens the shame associated with their financial burden.

5. Depression

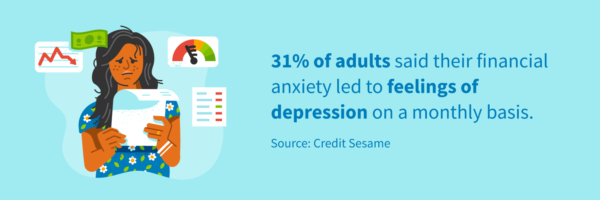

No one has ever been thrilled about a low credit score—but for some, it can lead to bouts of depression that keep them from fully living their lives or managing their money more responsibly. In 2020, 31 percent of American adults reported their financial anxiety led to feelings of depression on a monthly basis.

Given the significant limitations that come with debt or a bad credit score, it’s unfortunately unsurprising how it can wreak havoc on one’s mental health. A contributing factor to this could also be a lack of knowledge on how to turn their poor credit score around: A 2020 survey found that 16 percent of respondents with poor credit said their credit score makes them feel confused. When asked how their credit score has hurt them in life, 24 percent of poor credit-carriers said they’ve never learned to successfully navigate the financial system.

The consequences of financial hardship alone are enough to seriously damage one’s mental health (48 percent of adults in debt said it negatively impacted their optimism in 2019). But coupled with a lack of understanding of how to fix it no doubt leads to intensified feelings of hopelessness. After all, 43 percent of indebted adults said their debt negatively affected their sense of direction.

6. Self-esteem

Whether we like it or not, society has taught us to tie our self-worth to the amount of money we have in the bank. A 2019 study of individuals in debt revealed that respondents felt less self-confident due to their inability to adequately save money and protect themselves from unforeseen financial burdens. That same study found that 51 percent of respondents in debt didn’t feel as though they made the most of themselves.

When people feel a lack of confidence and self-esteem due to their poor credit heath or debt, it’s not unusual for them to avoid taking the steps necessary to rebuild their credit and find a more solid financial footing. This can put a wedge between one’s ability to ever attempt building more sound credit habits, which just perpetuates their low self-esteem: 16 percent of Americans in a 2020 study reported feeling worried about facing the financial details of their lives.

When you look at another 2019 study that indicates 9 percent of respondents lost their home and 7 percent were unable to get a job due to credit card debt, it makes sense that the inability to sustain such major life milestones would directly impact one’s sense of self-worth.

7. Regret

Regardless of your credit health, most of us can think of a time when we felt regret over a purchase or financial decision—a 2019 Bankrate study found that 76 percent of Americans have a regret related to their finances. The study also found that 16 percent of Americans cited racking up too much credit card debt as their top financial regret.

Another Bankrate study found that 13 percent of employed Americans put off saving money due to the amount of debt they carry. A lack of savings can be a major financial setback—when an unexpected event or emergency occurs and you have no savings to cover it, this only leads to more regret.

It’s typical for people to feel intimidated or overwhelmed by the situation that resulted in feelings of regret in the first place—whether it’s the amount of debt they owe, the significant drop in their credit score or their passivity in saving—and thus put off confronting it. This keeps the cycle of regret in motion, and it’s a tough spot that many have unfortunately found themselves in.

8. Anger

While some are thrust into feelings of depression over their poor credit scores, others experience the negative effects of anger as a result. A 2020 Credit Sesame report cited that 30 percent of individuals with poor credit felt angry because of it.

The same study found that 28 percent of individuals with poor credit couldn’t rent the apartment they wanted; 49.5 percent couldn’t qualify for an auto loan; 21.6 percent couldn’t lease a cell phone; and 19 percent had to live with their parents longer than they would’ve liked. It’s easy to see why bad credit could inevitably lead to feelings of anger or resentment due to the negative circumstances it often results in.

9. Work performance

In 2020, 19 percent of adults said their financial burdens impacted their job performance on a monthly basis. This could be due to the other negative side effects associated with bad credit previously mentioned such as lack of sleep, increased stress or high levels of anxiety that leave them distracted and unable to fully focus at work.

In 2019, a Credit Sesame study showed that 7 percent of individuals with bad credit were unable to get a job because of it. This is likely due to the fact that employer background checks may involve a request to review your credit history. If your credit report shows proof of a bad credit score, it could make employers hesitant to hire you—some hiring managers will equate your lack of financial responsibility with your ability to meet standards and expectations at work.

10. Strained relationships

Dealing with the consequences of a bad credit score and an overall unstable financial situation can quickly lead to strain in personal relationships. In a 2019 study, 36.1 percent of divorced participants indicated financial problems were a large contributor to higher levels of tension in their relationship. Additionally, another 2019 study found that 8 percent of respondents have broken up with or divorced their partner as a result of credit card debt.

If your partner brought their bad credit score or large amounts of debt into the relationship, it’s not unusual for this to lead to feelings of resentment or blame towards that person when financial problems inevitably arise. Credit Sesame’s 2020 report cited that 10 percent of respondents admitted to having problems in romantic relationships because of bad credit. Similarly, if you’re carrying a bad credit score while also supporting family members who are monetarily dependent on you, it could lead to ill feelings against them as a way to cope with your debt.

4 ways improving your credit may improve your wellbeing

Working towards improving your credit is a worthwhile goal that will help you in many major aspects of your financial life. Lower interest rates, better loan terms, and the ability to afford unexpected emergencies are just a few of the ways a higher credit score can support you financially. But improving your credit score could have a positive impact on more than just your finances.

Paying less interest frees up income for wellness-related expenses

There’s always a cost to borrowing money, whether you’re taking out a loan or opening up a new credit card. This shows up as the interest rate a lender will offer in exchange for approving you for borrowed funds. But that interest rate is significantly impacted by your credit score, and if your score is low, you might find yourself putting all your extra income towards those interest fees every month. Your low credit score indicates a risk to lenders, and they won’t readily loan you money without tacking on a hefty fee to make it worth their while.

That said, if you take steps toward improving your credit and raising your score, you’ll find yourself paying far less in interest fees and dealing with monthly rates that are actually manageable. This frees up your wallet to invest more in your health. Whether that means being able to afford weekly therapy, a gym membership or a different wellness-related expense, the money saved on interest alone is bound to lower your stress.

Stress less with a lower credit card balance

Speaking of lower stress, if you’re one of the 73 percent of Americans who lose sleep at night due to a financial issue (or one of the 13 percent losing sleep because you’re wondering if you’ll be able to pay your credit card debt), part of improving your credit score involves paying down your debt and lowering your credit utilization ratio.

Your credit utilization ratio is the amount of money you borrow compared to your maximum credit limit. If you’re constantly borrowing money, your utilization ratio will be high and lower your credit score. But if you focus on paying down debt and lowering that ratio, you won’t feel a wave of stress every time you think about the balance you owe on your credit card. You might find yourself sleeping easier at night when you no longer lie awake thinking of the high balance on your credit card statement.

Soften the blow of unexpected healthcare emergencies

If you’re concerned about healthcare costs, you’re not alone—Americans cited the increasing cost of healthcare as their top financial concern in 2020, and 77 percent said the cause of their financial anxiety was the possibility of a health emergency.

If you work towards improving your credit score by paying down your debt as quickly as possible—thus lowering your credit utilization ratio and raising your score—a health emergency won’t be as devastating a blow to your wallet should it arise. Ideally, by paying down your debt, you’ll have more money available to put into savings for such occasions. But even without the extra savings, improving your credit score will lower the cost of any loans you may have to take on in order to cover the costs of a health emergency.

Educating yourself financially improves self-esteem

If you decide to embark on the journey of improving your credit, you’ll have to start by learning the process and understanding what steps are involved in raising your score. This can be intimidating if you’re one of the poor-credit carriers who have never learned to successfully navigate the financial system.

But taking ownership of your financial life will ultimately give you a new sense of accomplishment that could drastically change your self-esteem when it comes to money. Avoiding it only perpetuates your lack of confidence, but choosing to do the work to raise your credit score can ultimately breed new levels of personal success.

A bad credit score unfortunately follows you everywhere, and can negatively impact some of the most critical parts of your life. Buying your first home, purchasing a car, taking out a loan or saving for retirement will all come with more barriers—and far higher rates and premiums—if your credit score isn’t where it should be.

When these negative impacts start to have ramifications on your physical and mental wellbeing, it can be tough to cope. But working towards improving your score while implementing time for self-care will lead you to a healthier and happier place—for your mind and your wallet.

To learn more about how your credit score impacts some of life’s most important milestones and guidance on how to start building better credit, consider a consultation with a credit repair advisor who can walk you through the process.