Disclosure regarding our editorial content standards.

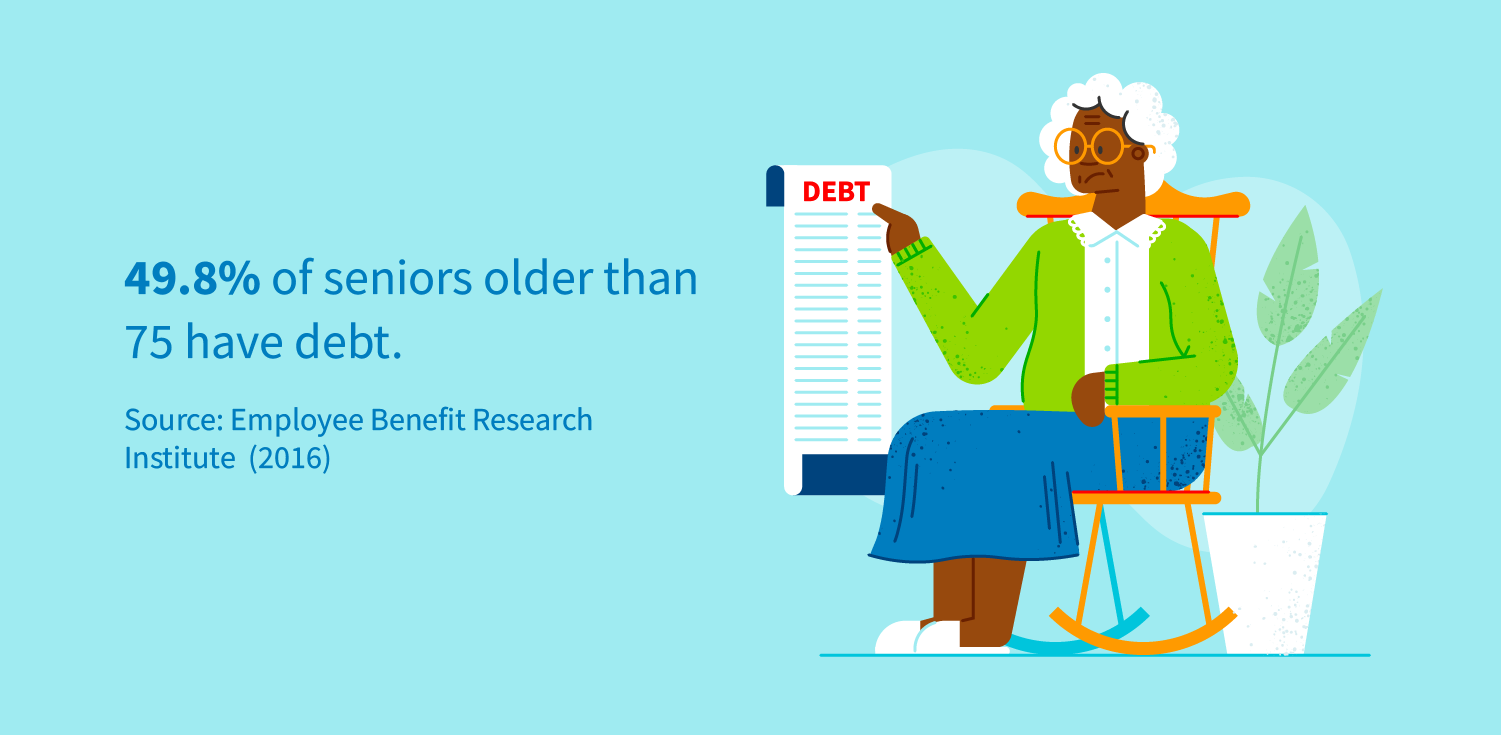

They say you can’t take anything with you when you die, so what happens to your debt you’ve left behind? Let’s just say your debt doesn’t die with you. In a study conducted by Credit.com, they found that most Americans (73 percent) die with debt like student loans, medical bills or auto loans. Creditors will claim what is theirs by liquidating your estate.

However, if you die lacking sufficient assets in your estate to pay off your debt, you may just leave behind more than memories for your loved ones—you could leave a spouse or child with the responsibility of paying off your debt.

Read on as we take a look at what happens to your debt when you die. Check out our tips for handling your finances to prevent your loved ones from inheriting any unpaid debt.

Are your debts forgiven at death?

When someone dies with debt, it doesn’t go away. Typically, unpaid debts are settled with the person’s estate or owned assets, such as a house, as payment. An executor, representative or administrator of your will usually handles your estate finances. From there, they’re responsible for paying off debts with the money in the estate during probate—the legal process that makes sure property and possessions are given to the correct people.

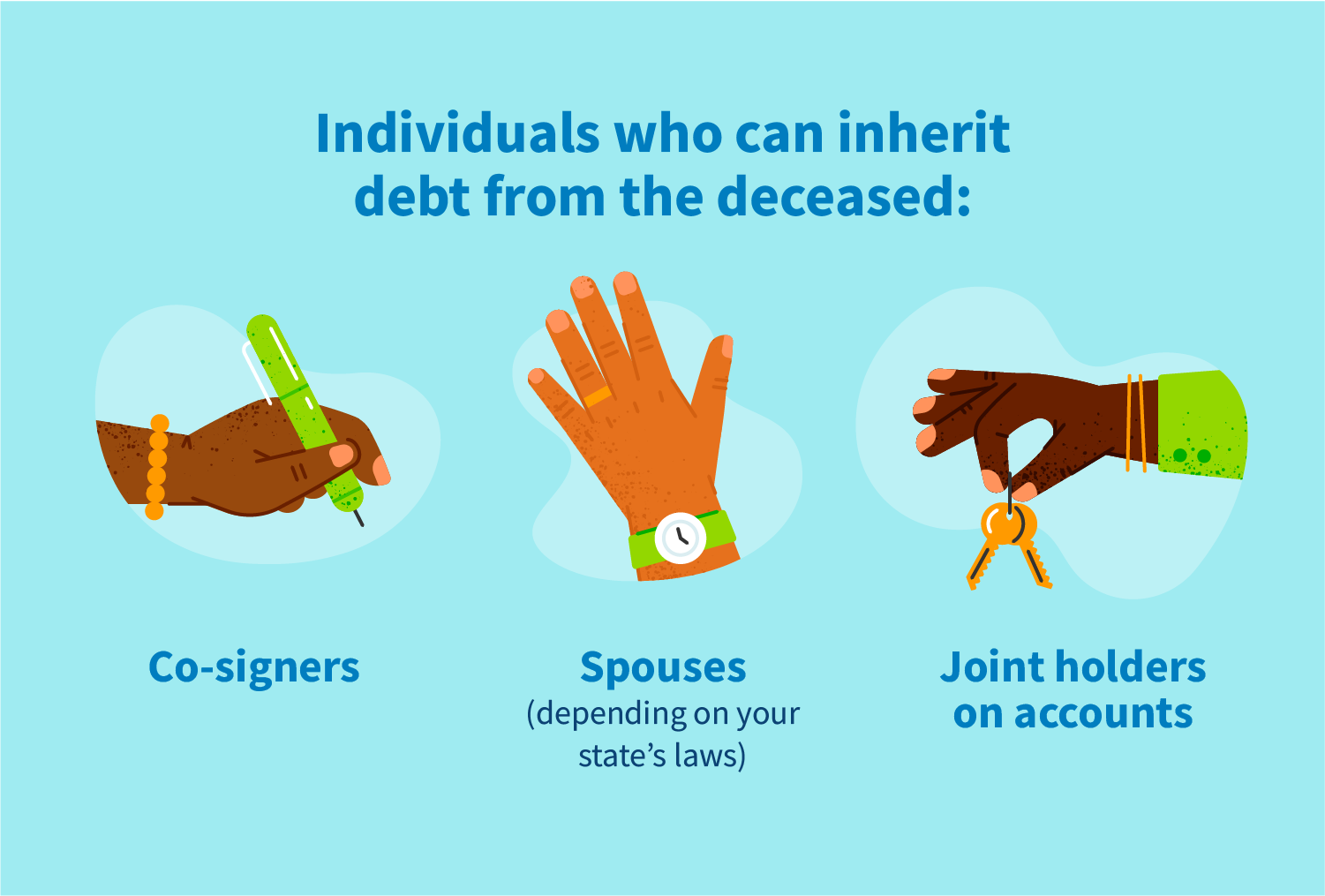

Who can inherit your debt?

Generally, if the debt of the deceased isn’t paid, you can only inherit it if your signature is on the account or loan. We’ve outlined a few people that may inherit debt below:

- Cosigners: Someone who has cosigned on a loan and is legally responsible for paying off the loan if you can’t.

- Joint holders on accounts: A person who is a joint holder or owner of an account with the deceased.

- Spouses in community property states: If you live in a community property state, where debt earned during marriage is considered community property or equally owned by spouses, your surviving spouse may be required to pay off the debts in the event that you leave behind debt. The following are community property states: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin.

What happens to different types of debt?

Exactly how a debt is paid after someone dies depends on the type of debt, where they live and whose signatures are on the loan. Review these common debts and how they may be settled if the account holder passes away.

Student loans

Since a federal student loan typically does not require a cosigner or another person on the account, it can be canceled upon the borrower’s death. However, private student loans aren’t always canceled in the event that the borrower dies as they usually require a cosigner. If the borrower dies, the cosigner of a private student loan could be responsible for settling the debt.

Medical bills

Medical bills are on a high priority list of bills that need to be settled when someone dies with this type of debt. So, when someone dies with outstanding medical bills, the deceased’s estate assets will be liquidated to pay these bills off. If the deceased’s estate is not enough to pay off the bills, then the debt may fall on children under filial responsibility laws.

These are laws that put responsibility on adult children to support their parents. There are 30 states with filial responsibility laws.

Mortgage loans

Most mortgages are signed or borrowed by married couples. If this is the case when someone dies, the living spouse becomes the legal owner and can live in the house, sell it or refinance. If they want to continue to keep the house, they will have to make the mortgage payments.

If the living spouse is not on the mortgage loan, they may not have rights to the house in the event that the account holder on the mortgage loan dies. However, in your will you’re able to assign a beneficiary. This person will inherit the title of your house once you have passed and will have legal responsibility to make decisions for the house.

If the house is not inherited or there are no payments covering the mortgage, a lender can take possession or foreclose on the home.

Credit card debt

If an individual dies with auto loan debt, their family members could inherit it. Like other loans, if there’s a cosigner on it, that person will be responsible for settling the debt. Spouses in community property states may also be legally obligated to handle the balance as well.

In the event where there is no cosigner, heirs are able to purchase the vehicle and pay off the debt or return the vehicle to the lender. If there is any money that is still owed on the car, even if it’s sold, the lender may try to collect the outstanding balance from the deceased’s estate.

What can creditors take?

When someone dies with credit card debt, the creditor will submit a claim against the deceased’s estate to settle the debt.

If the deceased does not have enough assets to pay off their debt, they’ll likely try to find other ways to get the money that’s owed to them. That said, they’re not allowed to go after the family of the deceased for repayment unless they’re legally responsible for the debt (cosigner, joint holder on the account, etc.).

Additionally there are limits on what they can take to settle the debt—life insurance benefits, trust funds and most retirement accounts are protected.

How to protect your family from inheriting your debt

The easiest way to protect your family from inheriting your debts is to have a sufficient life insurance policy. If this policy has been maintained over the years, it may be able to pay all your debts when you pass, leaving no burden on your spouses, children or heirs. A life insurance policy will also distribute your estate to designated heirs and beneficiaries based on your written wishes.

Having an updated will outlining how debts will be paid can also save your family from inheriting your debt. Finally, avoiding situations where you have a cosigner or joint account holder could protect your family from debt inheritance.

Each state has a priority list of how debts will be paid, typically with medical expenses and unpaid taxes having a higher priority than credit debt. Any other remaining debt that can’t be paid off through an estate, cosigner, joint account holder or spouse will have to be written off by the creditors—meaning the creditor decides there is little or no chance of collecting the debt and writes it off as a financial loss.

If a loved one has passed and you’re concerned about how it may impact your own credit score, speak with our credit repair team to learn how to protect your financial health.

Source: https://www.credit.com/blog/americans-are-dying-with-an-average-of-62k-of-debt-168045/

Source: https://www.credit.com/blog/americans-are-dying-with-an-average-of-62k-of-debt-168045/Source